China is slowly changing its reliance on export to more of a domestic consumption focus. One such company which may be able to ride on this domestic consumption story is Eratat Lifestyle. (“Eratat”)

Description of Eratat

Eratat started as a sports shoe / sportswear company and moved into the design and distribution of lifestyle fashion apparel under its proprietary brand “ERATAT” (“ 鳄莱特”) about 3-4 years ago. Please refer to their company website

http://www.eratatgroup.com/v2/ for more information.

Investment merits

1. Near term results likely to be better without once off items

Eratat recognised a once off sales incentive in 4QFY11 of RMB51.7m and renovation subsidy RMB41.8m in 1HFY12. Without these once off items, it is reasonable to assume that 4QFY12F and 1HFY13F results are likely to better off on a year on year comparison.

2. Strongest catalyst : new distributors

Eratat has been in talks with new distributors via their 100%-owned subsidiary in Shanghai. Discussions have been ongoing for a few months and they are likely to materialise this year. However, impact is likely to be seen in 2HFY13F and (perhaps) more so in FY14. This is likely to be the strongest catalyst for the company.

3. Right industry, albeit competitive

Eratat is in the right industry and based on China’s macro outlook, the retail industry is likely to ride on the wave of domestic consumption and do well over the next couple of years.

4. Active investor relation efforts

Both Ken Ho, CFO and Kellyn Tan, Eratat’s investor relation (“IR”) have been active in doing IR activities. Unlike other S chips who may be discouraged (due to their low company share price despite their efforts) and stop meeting people, Eratat CFO and IR have been actively engaging the investment community despite their low share price last year.

5. Net cash per share of 15.7 SG cents

Eratat has no outstanding loans and according to the management, they do not have any bad debts on their accounts receivables for the last five years. For the net cash of 15.7 SG cents, it is noteworthy that the net cash fluctuates. They are usually lower in 2Q and 4Q as a significant amount of cash would be placed as trade deposits to their apparel manufacturers to secure delivery of their apparel products.

Investment risks

As with all investments, there are some noteworthy points to take note:

1. Possibility of equity raising

Readers who have been following Eratat understand that Eratat requires significant working capital for their apparel business. Eratat outsources the manufacture of their apparel products to mid or large sized third party manufacturers. These third party manufacturers concurrently manufacture apparel products for high end local and international brands. In order to secure delivery of products, Eratat has to place 50-60% as trade deposits at the time of placing orders with them. (They do not have their own apparel manufacturing facility because their current size does not warrant them to have their in house facilities.) In order to expand faster in their apparel business, it is likely that company may need to raise more cash for their working capital requirements.

2. Usual S chip risks apply

Besides the usual corporate governance risk surrounding S chips, they also face liquidity risk and price risk. Although sentiment has improved since last year, it is still rather fragile. (I believe most investors would still sweat whenever the S chips that they hold halt trading) Eratat’s liquidity has improved markedly since mid Dec 2012 but its average 30D and 100D EMA volumes are still at modest levels of around 2.3m and 1.3m of shares respectively.

Valuations – 2.3x FY13F PE; NAV / share ~ $0.355

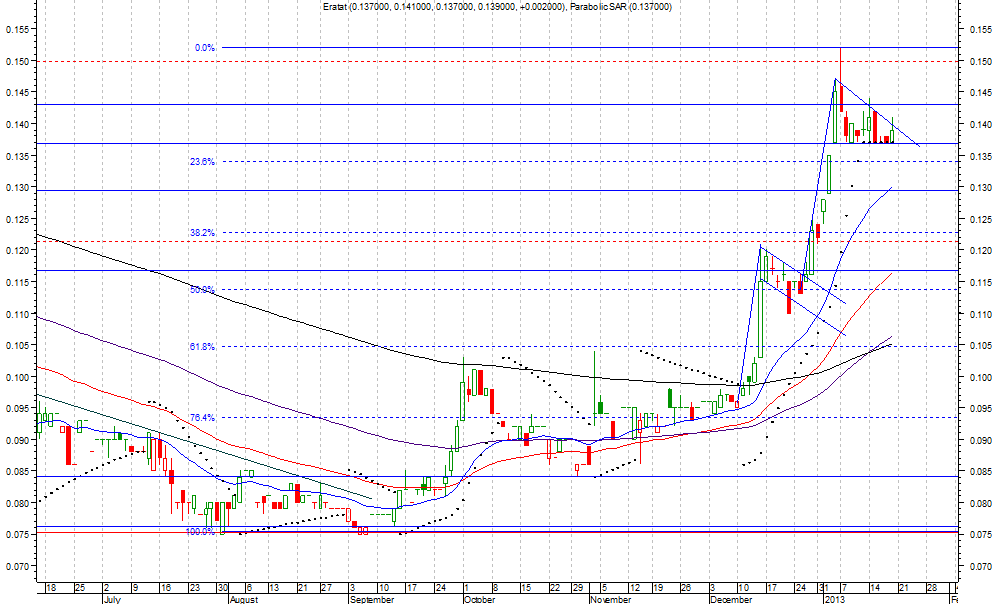

Based on Chart 1 below, Eratat has surged 74% from the low of around $0.080 in July – Sep 12 to $0.139 on 18 Jan 13. However, its valuations do not appear to be excessive. It trades at around 2.3x FY13F PE. NAV / share is approximately $0.355. Estimated yield is 3.0%. SIAS covers this company with a one year target price of $0.240.

Chart 1: Eratat price has jumped 74% since the low in July – Sep 12

Source: Metastock as at 18 Jan 2013

Readers who are interested can email me at

crclk@yahoo.com.sg for their financial statements or / & research reports.

*This is an amended version which I have sent out to my clients on 19 Jan 2013, Saturday.

Disclaimer

The information contained herein is the writer’s personal opinion and is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided herein do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or invest in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein are suitable for you. The writer will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials appended herein. The information and/or materials are provided “as is” without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Hi Ernest,

I am a retail investor in Singapore stocks, and a retiree. I happened to read your interesting report on Yamada that you wrote sometime in April last year. The stock is now traded around S$0.13 and the company's performance in the last 2 quarterly appeared to be disappointing. What is your view about this stock in the near and midium term.? Is it still an attractive stock to get in at the current price?

Best regards

C.S.Tan

Hi CS

Thanks for your comment. Apologies for taking so long to reply as i only saw it. Guess you should already have your ans after Mr Sam Goi invested in Yamada. Hope you have got some Guocoleisure after my writeup on 17 Feb.

Going forward, you may wish to drop me an email at crclk@yahoo.com.sg for speedier response.

Thanks and have a good weekend!

Cheers

Ernest

Thanks again for the article post.Much thanks again. Great.

Major thanks for the article.Really looking forward to read more. Cool.

I truly appreciate this blog.Thanks Again. Want more.

Hey, thanks for the blog. Awesome.

I really like and appreciate your article post.Thanks Again. Great.

Enjoyed every bit of your blog post.Much thanks again.

Fantastic article.Thanks Again. Great.

Great article post.Really thank you! Keep writing.

Looking forward to reading more. Great article post.Much thanks again. Really Cool.

This is one awesome blog post.Much thanks again. Keep writing.

Thanks-a-mundo for the post.Really thank you! Cool.

Enjoyed every bit of your article post. Really Cool.

Thanks for the blog.Really looking forward to read more. Want more.

Im obliged for the blog post.Much thanks again. Really Great.

Great post. Want more.

Say, you got a nice blog.Really looking forward to read more. Fantastic.

I really enjoy the blog.Really looking forward to read more. Want more.

Im obliged for the post. Want more.

Thanks for sharing, this is a fantastic blog post.Really thank you! Much obliged.

This is one awesome post.Really looking forward to read more. Much obliged.

A round of applause for your post.Thanks Again. Great.

Im thankful for the post.Really looking forward to read more. Will read on…

Major thankies for the post.Thanks Again. Want more.

A round of applause for your post. Really Great.

I think this is a real great article.Really thank you! Cool.

Major thanks for the article.Really looking forward to read more. Awesome.

Enjoyed every bit of your blog article.Thanks Again. Keep writing.

I truly appreciate this blog.Thanks Again. Fantastic.

Wow, great article post. Fantastic.

Really informative post.Really thank you! Fantastic.

Thanks for the blog article. Fantastic.

Thanks so much for the article post.

Great, thanks for sharing this article post.Much thanks again. Want more.

Im obliged for the post.Really looking forward to read more. Fantastic.

Awesome article.Really looking forward to read more. Really Great.

wow, awesome blog.Thanks Again. Want more.

I value the article. Awesome.

Very informative blog.Really thank you! Cool.

I appreciate you sharing this article.Really looking forward to read more. Really Cool.

A big thank you for your blog article.Really looking forward to read more. Really Cool.

Very informative post.Really looking forward to read more. Fantastic.

A round of applause for your article.Much thanks again. Awesome.

Really appreciate you sharing this blog post.Really thank you! Great.

Looking forward to reading more. Great blog post. Awesome.

I loved your article post. Much obliged.

A round of applause for your blog article. Fantastic.

I value the blog article.Thanks Again.

Very good blog post.Really thank you! Will read on…

Appreciate you sharing, great blog post. Great.

Really enjoyed this article post.

Really appreciate you sharing this blog post.Much thanks again. Much obliged.

I really enjoy the blog. Much obliged.

Thanks again for the blog article.Really looking forward to read more. Awesome.

Great, thanks for sharing this article post. Great.

This is one awesome post.Really thank you! Want more.

Awesome article post.Thanks Again.

Fantastic blog post. Much obliged.

Im thankful for the post.Thanks Again. Much obliged.