Amid the backdrop of the recent market weakness, I have done my personal compilation of stocks whose past year Price to Book Value (“P/BV”) are lower than their average five year P/BV (see my http://ernest15percent.com/index.php/2015/09/11/ernests-market-outlook-14-sep-2015/ for more information.) I noticed that Ying Li International Real Estate Limited (“Ying Li”) past year P/BV is only 0.38 and is significantly below its average five year price to book of around 1.19. However, as there is no recent rated coverage on Ying Li, I have left out Ying Li in my personal compilation of stocks above. Notwithstanding this, Ying Li looks interesting and I decide to take a closer look in this company.

Company description

Ying Li is the first Chongqing-based property developer to be listed in Singapore. It is engaged in the development, sale, rental, management and long-term ownership of high-quality commercial and residential properties in prime locations in Chongqing.

Established in 1993, Ying Li has a solid track record in urban renewal, having transformed old city areas into high-quality and premier-design developments. Ying Li has modernized the landscape of Chongqing’s main business districts with the development of several landmark commercial buildings, such as New York New York, Zou Rong Plaza, Future International and Ying Li International Financial Centre.

So what attracts me to take a closer look?

China property sales may rise on the back of China’s easing policies

China’s property sector comprise of approximately 25 – 30% of China’s GDP (if we include the upstream and downstream industries such as such as appliances, cement, furniture, glass and steel etc.). In view of the slowing economy, China has cut both the benchmark interest rates and the banks’ required reserve ratio four times since the start of 2015. In addition, China has reduced the minimum down payment for 2nd home buyers to 20% and also allows foreigners to buy property in China, subject to conditions. All of the aforementioned easing measures are likely to bode well for the property market.

FY16F results likely to be better than FY15F

Based on Ying Li’s existing pipeline of projects, it may see a better FY16F vis-à-vis FY15F due to potential contributions from property sales in San Ya Wan Phase 2 and IEC Phase 1. Rental income may also improve in FY16F vs FY15F due to change in tenant mix, increase occupancy rate and improvements from asset enhancement initiatives in some of their properties.

Becoming more transparent

Ying Li has started to be more transparent with more regular updates to shareholders in terms of company updates. This can be seen in their spate of press releases since Jul 2015 where they updated shareholders on their Ying Li iMIX parks, Beijing Tongzhou and IEC projects.

In addition, in a bid to showcase their properties to the investment community, Ying Li is hosting an analyst site visit from 15 Sep – 18 Sep. This is the first site visit in at least two years. It will be interesting to see whether there will be any reports or updates after the site visit (bearing in mind that there is no rated coverage at the moment.)

CEO purchase, the first in at least four years

Mr Fang Ming, Executive Chairman and Group CEO of Ying Li recently bought 1M shares @$0.126 on 25 Aug 2015. This was the first purchase in at least four years. Although the amount is not extremely significant, it is still a good vote of confidence by the management.

China Everbright Limited’s 14.9% stake in Ying Li is reassuring

Based on Ying Li’s annual report 2014, China Everbright Limited (“CEL”) holds around 14.9% of Ying Li’s shares. CEL is part of the China Everbright Group which is one of the larger state-owned enterprises in China. Thus, CEL’s investment in Ying Li is reassuring to a certain extent as such state owned company is likely to have done extensive checks on Ying Li and their key management. It is noteworthy that CEL’s investment cost for its 14.9% stake in Ying Li is at $0.260.

Depressed valuations

Ying Li’s depressed valuation is the first thing to catch my attention. According to Bloomberg, Ying Li’s past year P/BV is only 0.38 and is significantly below its average five year price to book of around 1.19x. For the past five years, Ying Li trades between 0.23x – 2.02x P/BV.

Furthermore, on a PE comparison, according to Bloomberg, Ying Li trades at a historical PE of around 7.4x and is also at the lowest end of the PE range of 7 – 134x. (See Chart 1 below)

Chart 1: Ying Li PE at the low end of its 5 year PE range

Source: Bloomberg

It is noteworthy that in times of capitulation or extremely weak market conditions, it is entirely possible that Ying Li may trade lower than its P/BV of 0.38x and PE of 7.5x. What we know for now (based on statistics) is that, Ying Li is trading at levels at the lower end of their historical valuation bands. Ceteris Paribas, when sentiment recovers, coupled with Ying Li’s continued delivery of good results and property sales (be it in the coming months or years), it is likely that it may re-rate nearer to their historical means.

Risks

China’s property market is still challenging

According to the China Index Academy, new home prices in China saw their first year on year increase in August 2015, the first in 11 months. Thus, China’s property market continues to be challenging despite the above China’s easing measures.

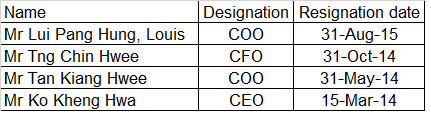

Key management changes since 2014

With reference to Table 1 below, since 2014, there were some notable management resignations. For example, there were high hopes when Mr Ko Kheng Hwa, previously CEO of Singbridge and JTC Corp, when he joined Ying Li in 2013. However, he resigned in 2014 citing personal reasons. Both Mr Tan Kiang Hwee and Mr Lui Pang Hung quitted their role as COO in one year or so. This rapid movement in key management bears watching as it may be a potential red flag.

Table 1: Key management changes since 2014

Source: SGX; Ernest’s compilations

Despite the management shuffles, it is noteworthy that Mr Lim Gee Kiat re joined Ying Li as their CFO. He was the ex Senior Vice President, Finance of Ying Li from 2011 – 2013. Mr Lim has an illustrious record as he was the CFO of Nera Telecommunications (Listed on Singapore Mainboard with a market capitalization of S$215m) from 2013 to 2015. He was VP of GIC Special Investments from 2007 – 2011.

Lumpy quarterly results

As a developer, Ying Li’s quarterly results are lumpy, in line with other property developers. Ying Li is cognizant of their lumpiness and seeks to smooth out this lumpiness by increasing their rental income proportion. This naturally takes time and we may be able to see their efforts in FY2016F.

Chart analysis

Ying Li has been entrenched in a strong downtrend since Apr 2015 with ADX at 55.0. ADX reached a recent high of 66.5 on 26 Aug 2015 and has fallen from such overextended levels. RSI reached an all-time oversold 13.0 on 24 Aug 2015 and have rebounded to 34.4 in tandem with the recovery in the share price. Coupled with a bullish moving average crossover in MACD, it is likely that the largest and sharpest decline in Ying Li’s share price may have already been over.

Near term supports: $0.133 / 0.128 / 0.125 – 0.126

Near term resistances: $0.143 – 0.145 / 0.153 – 0.157

Chart 1: Ying Li’s share price is below GFC levels

Source: CIMB chart as of 10 Sep 15

Conclusion

The above is a brief introductory write-up on Ying Li. Ying Li’s attractive valuations, upcoming analyst site visit and updates on their property sales are some interesting and potentially positive factors. However, the still challenging property market, lumpy results and high turnover at key management levels are noteworthy factors for readers to take into consideration. Readers can refer to Ying Li’s corporate website http://www.yingligj.com/ for more information.

Disclaimer

Please refer to the disclaimer here http://ernest15percent.com/index.php/disclaimer/ .

I really enjoy the blog article.Thanks Again. Really Great.

I am so grateful for your article post.Much thanks again. Keep writing.

Thank you ever so for you blog article.Really thank you! Fantastic.

Hey, thanks for the blog post.Really thank you! Fantastic.

Hey, thanks for the article.Really looking forward to read more. Awesome.

Enjoyed every bit of your blog. Cool.

Thanks for the post.Much thanks again. Keep writing.

I really enjoy the blog.Much thanks again. Much obliged.

Major thankies for the post.Thanks Again. Really Great.

Wow, great article.Really looking forward to read more. Really Cool.

Great, thanks for sharing this post.Much thanks again. Much obliged.

Looking forward to reading more. Great post.Much thanks again. Great.

Thanks so much for the article post.Much thanks again. Really Cool.

Appreciate you sharing, great blog.Much thanks again. Want more.

Enjoyed every bit of your blog article.Thanks Again. Awesome.

Very good blog post.Really thank you! Really Cool.

Great article post.Really looking forward to read more. Want more.

Awesome article.Really thank you! Want more.

Awesome blog post.Much thanks again. Cool.

Hey, thanks for the blog post. Cool.

Very informative blog post.Really thank you! Will read on…

Muchos Gracias for your blog.Really looking forward to read more. Really Cool.

Thank you for your blog post.Much thanks again. Will read on…

Im obliged for the blog article.Much thanks again. Great.

Thanks a lot for the blog post.Really looking forward to read more. Will read on…

Hey, thanks for the post.Thanks Again. Really Cool.

Im obliged for the blog article. Much obliged.

Im grateful for the blog.Really looking forward to read more. Much obliged.

Very informative article post.Much thanks again. Awesome.

A round of applause for your blog article.Much thanks again. Awesome.

Thanks a lot for the article.Thanks Again. Cool.

Fantastic blog post. Really Cool.

Very informative post.Thanks Again. Really Cool.

Very good blog post. Great.

Looking forward to reading more. Great article post.Really looking forward to read more. Great.

I value the blog.Much thanks again. Great.

Great, thanks for sharing this blog article.Really looking forward to read more.

I loved your blog article. Fantastic.

Major thanks for the blog.Much thanks again. Much obliged.

Major thanks for the blog article.Really thank you! Great.

Great, thanks for sharing this blog.Really thank you! Really Cool.

Great blog.Really looking forward to read more. Cool.

Appreciate you sharing, great blog.Much thanks again. Really Cool.

Hey, thanks for the blog.Thanks Again. Cool.

Thank you for your blog article.Thanks Again. Really Cool.

Muchos Gracias for your article post.Really thank you! Much obliged.

Thank you for your blog.Really thank you! Great.

Wow, great blog article.Really looking forward to read more. Much obliged.

I cannot thank you enough for the post.Thanks Again. Really Cool.

Major thankies for the post.Thanks Again. Great.

Very good article.Thanks Again. Really Cool.

Hey, thanks for the post.Much thanks again. Cool.

I appreciate you sharing this article.Thanks Again. Really Great.

Thank you ever so for you article post.Thanks Again. Really Great.

I value the blog.Much thanks again. Keep writing.

Great, thanks for sharing this blog post. Keep writing.

Really informative blog post.Really looking forward to read more.

Major thankies for the blog.Much thanks again. Keep writing.

Looking forward to reading more. Great blog post.Really thank you! Will read on…

Really informative blog article.Much thanks again. Fantastic.

Can someone recommend Glass Dildos? Cheers xxx

I really enjoy the article.Thanks Again. Will read on…