From AI Hardware to Internet Giants: Is It Time to Revisit Hang Seng Tech? (3 May 2026)

Dear all,

The Hang Seng Tech Index (HST) has corrected sharply—falling 27% from its multi-year high of 6,715 (2 Oct 2025) to 4,871 as of 30 Apr 2026. Notably, it now sits just 148 points above its pre–DeepSeek level (4,723 on 28 Jan 2025).

This raises an important question:

Is capital about to rotate from crowded AI hardware trades into overlooked internet giants?

Both CGSI and UBS think this is increasingly likely. Here’s a breakdown of the investment case.

Investment Case (7 Key Points)

1) Underperformance may be creating an entry point

HST has lagged both regional peers and A-shares, largely due to its limited exposure to the AI hardware rally.

- Past 1 month:

- ChiNext: +11.9%

- STAR50: +14.8%

- HST: +2.8%

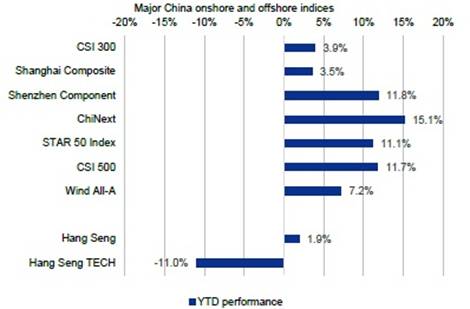

If we were to compare year-to-date (YTD) performance (See Fig 1), HST underperformance is stark, down 11% with all the other indices posting positive YTD performance.

The performance gap is now hard to ignore.

Figure 1: YTD performance of HST vis-à-vis the other China indices

Source: CGSI Research; Wind with data as of 29 Apr 2026

2) AI hardware trade looks increasingly crowded

The A-share AI supply chain rally (semiconductors, optical, GPUs) is becoming highly concentrated.

As of Apr 2026,

- Top 25 stocks = 0.5% of listings

- But account for 11.7% of total turnover (Apr 2026)

- 3rd highest concentration in 2 years

This raises the risk of profit-taking and rotation.

3) Rotation into “soft tech” could benefit HST

As hardware trades mature, capital may rotate into:

- Internet platforms

- AI application companies

HST is well-positioned here:

- ~52% exposure to internet names

- Valuation discounts vs ChiNext and Nasdaq have widened to levels last seen in Sep 25

- Index has reset to pre-DeepSeek levels

4) Valuations look compelling

Relative valuations vs:

- A-shares

- US tech

…have widened to historically attractive levels, improving risk-reward for a tactical rebound.

5) External tailwinds are turning supportive

- S&P 500 and Nasdaq at highs

- Renewed interest in US software (IGV)

- HST has ~0.8 correlation with US software

If this trend persists, it could spill over positively into HST.

6) Multiple near & mid-term catalysts:

Potential triggers include:

- 🤖 Potential for renewed optimism towards new AI developments (DeepSeek, Tencent Hunyuan LLM)

- 🚗 Strong EV demand (autos ~16% of HST) should oil prices remain high

- 🍔 Alleviating food delivery competition in upcoming quarterly results

- 🤝 Potential easing of US–China tensions (Trump’s planned China visit mid-May) (see HERE)

- ⚖️ Possible resolution of Trip.com anti-trust probe

7) High-conviction names: Platform leaders

Within the index, Tencent and Alibaba stand out due to:

- Dominant ecosystems

- Strong positioning in AI + internet applications

- Leverage to any sentiment recovery

Key Risks to Watch

No investment case is complete without the risks. Examples of some obvious risks are

1) China policy and regulatory risk

While less aggressive than 2021–2022, policy risk has not disappeared.

👉 Example: Trip.com anti-trust probe (Jan 2026)

2) AI capex arms race (uncertain ROI)

- Heavy investment across Chinese tech firms

- Risk of margin compression

- Uncertain near-term monetisation

3) US–China tensions remain a structural overhang

U.S. China risks continue to be a sword of Damocles over the China tech recovery story.

Key concerns include:

- Export controls on semiconductors

- Taiwan-related risks

- ADR delisting / capital restrictions

Even without escalation, this supports a persistent valuation discount.

4) Weak domestic macro backdrop

To some extent, China’s recovery hinges on a recovery in its property sector and domestic spending. China tech earnings especially e-commerce and fintech are still highly correlated to domestic consumption

China’s recovery remains uneven:

- Soft consumer confidence

- Property sector weakness

- Youth unemployment concerns

Without a clear macro inflection, earnings upgrades may not materialise.

Conclusion

The risks surrounding HST—regulatory uncertainty, geopolitics, AI spending, and macro weakness—are real and largely known.

However, this needs to be weighed against:

- Sharp underperformance

- Improving valuations

- Potential rotation out of crowded AI trades

- Emerging catalysts

Taken together, these suggest a potential mean reversion opportunity may be forming.

Within the index, CGSI continues to highlight Tencent and Alibaba as preferred exposures.

Disclaimer

Every investor’s situation is different. Please consider your own risk appetite, portfolio exposure, and investment horizon before making any decisions. This article is for general informational purposes only.

If you require advice tailored to your circumstances, do consult your financial advisor or banker.

If you’d like to stay updated on my future write-ups or insights, you can sign up at http://ernest15percent.com. There may be a slight delay in emails, as more detailed updates and information are usually shared with my clients first. For example, I have shared Oiltek, OKP and Nanofilm to my clients when they were trading around $0.700, $0.640 and $0.580 respectively last month. Prices move up too fast to have time to do a formal write-up on my blog. 😛

For those interested in working together, feel free to reach out at ernestlim15@gmail.com.

Please refer to the disclaimer HERE