UltraGreen.ai (ULG) – Time to Revisit the Story? (6 Jul 2026)

Dear all,

Following my write-up on 18 May 2026 (click HERE), UltraGreen.ai (“ULG”) declined to a low of US$1.18 on 19 May before rebounding approximately 22% to close at US$1.44 on 5 June. Many of us took some profit following the rebound.

Since then, the share price has retraced by about 16%, touching a low of US$1.21 on 2 July before closing at US$1.27 on 3 July.

With ULG’s 1HFY26 results expected in August, is it worth taking another look? In my view, the company remains worth monitoring as several potential catalysts could help address investors’ recent concerns.

For readers unfamiliar with ULG’s business, you may wish to refer to my earlier LinkedIn post HERE for a brief overview of its operations before continuing.

Potential drivers

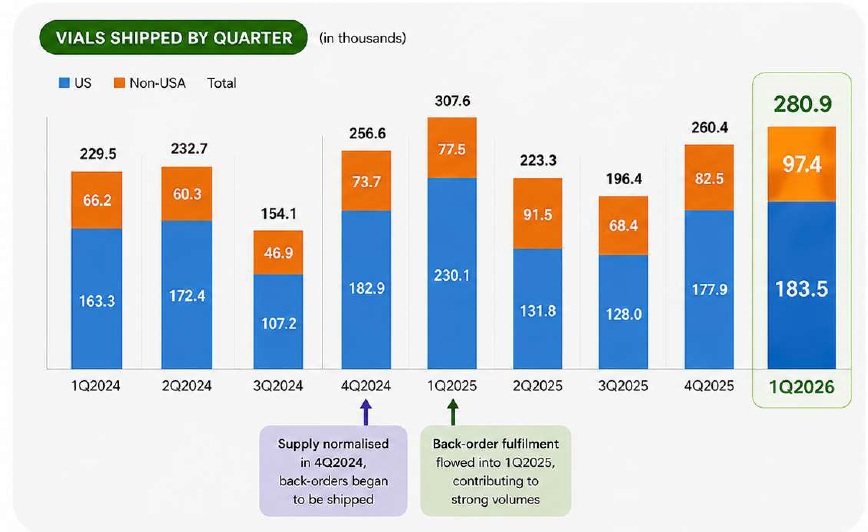

A) 1HFY26 results could help address growth concerns

The recent weakness in ULG’s share price followed its 1QFY26 business update. Although management provided an explanation (see Chart 1), some investors may be concerned that lower year-on-year shipment volumes could signal slowing revenue growth.

However, there are reasons to believe the situation may not be as negative as the market initially interpreted.

Firstly, management explained that 1QFY25 benefited from an unusually high comparison base due to the fulfilment of prior back orders.

Secondly, shipment volumes improved sequentially across both the U.S. and international markets during 1QFY26, suggesting that underlying demand remained resilient.

Annualising 1QFY26 shipment volumes of approximately 280.9K vials implies annual shipments of around 1.1m vials, representing roughly 14% year-on-year growth.

While annualising one quarter’s performance should always be interpreted with caution, management previously highlighted in its FY2025 Annual Report that the business generally does not experience significant seasonality because of the recurring nature of demand.

In addition, UOB Kay Hian’s report dated 5 May highlighted strong April sales, which appears broadly consistent with this view.

Chart 1: Number of vials shipped by quarter (in thousands)

Source: ULG

B) Analyst expectations remain constructive

According to Bloomberg consensus estimates as at 3 July 2026 (see Figure 1 below), analysts have an average target price of approximately US$1.98, representing around 57% upside from the current share price of US$1.27.

Separately, Phillip Securities initiated coverage on 29 June 2026 with a Buy recommendation and a target price of US$1.92 (click HERE). Including this report, the average target price rises to approximately US$1.99.

Interestingly, although management has guided FY26 revenue of approximately US$170m to US$190m, consensus revenue forecasts currently stand at around US$177m, which is below the midpoint of management’s guidance.

Should the company execute well during the remainder of the year, there could be room for earnings upgrades. Nevertheless, investors should remember that analyst target prices are estimates rather than guarantees.

Figure 1: Analyst target prices; Consensus TP: US$1.99 (~57% potential capital upside)

Source: Bloomberg as of 3 Jul 2026

C) Share buybacks and management purchases

Since commencing its share buyback programme on 28 May, ULG has repurchased approximately 992,500 shares across both its US$ and S$ counters.

The company bought shares at prices ranging from approximately US$1.23 to US$1.40 for its US$ counter.

Separately, CEO Ravinder Sajwan has also been purchasing shares in the open market. Since late May, he has acquired approximately 830,000 shares worth well over S$1m.

While insider buying and share buybacks do not guarantee future share price performance, they are generally viewed as positive signals that management believes the shares represent attractive long-term value.

D) Potential dividend policy announcement

Management previously indicated (click HERE) that it intends to communicate its approach towards dividends after gaining greater clarity on future investment requirements and balancing growth opportunities with shareholder returns.

Should the company introduce a formal dividend framework, it may broaden the stock’s appeal to a wider pool of institutional and income-focused investors. That said, investors should await further announcements rather than assume dividends will necessarily be introduced.

Key Risks Investors Should Monitor

As with any investment, ULG is not without risks.

Some of the more important factors that investors should continue monitoring include:

- Slower-than-expected adoption of Fluorescence Guided Surgery;

- Regulatory developments;

- Technology and competitive risks;

- Supply chain disruptions; and

- Execution risks associated with scaling the business.

Readers can refer to analyst reports HERE and my earlier write-up HERE to better appreciate the risks.

Conclusion

Despite the recent weakness in ULG’s share price, the latest business update does not necessarily suggest that the company’s longer-term structural growth story has materially changed.

Several potential catalysts—including the upcoming 1HFY26 results, continued execution, possible earnings upgrades, ongoing management share purchases and greater clarity on capital allocation—could help improve investor sentiment over time.

On the other hand, investors should continue balancing these potential positives against the execution, regulatory and adoption risks that remain inherent in the business.

As always, every investment carries risk. Investors should conduct their own due diligence and carefully consider their investment objectives, financial circumstances and risk tolerance before making any investment decision.

It will certainly be interesting to see how the company performs when it reports its 1HFY26 results in August.

Disclaimer

This article is provided solely for general information and educational purposes and should not be construed as financial advice or a recommendation to buy or sell any security.

Every investor’s financial circumstance, investment objective and risk tolerance are different. Please conduct your own due diligence and, where appropriate, consult a licensed financial adviser before making any investment decision.

I am vested in ULG.

If you would like to receive future write-ups, you may subscribe at my blog HERE.

As more detailed analyses are usually shared with my clients first, articles published on my blog may occasionally appear after the initial investment opportunity has emerged.

If you are interested in working together, feel free to contact me at crclk@yahoo.com.sg.

Please refer to the disclaimer HERE