UltraGreen.ai (ULG) – A High-Margin Healthcare Growth Story Still Intact? (18 May 26)

Dear all

Since April, UltraGreen.ai (ULG.SI) has seen its share price retrace 19% from an intraday high of US$1.54 on 27 April to an intraday low of US$1.25 on 18 May. More notably, the stock has fallen around 16% following its 1QFY26 business update — despite announcing regulatory approval for Verdye in Singapore.

This naturally raises a key question for investors:

Has the market overreacted, or has ULG’s growth story weakened materially?

In my view, the latest quarter still supports the broader investment thesis that ULG remains a compelling long-term healthcare growth story, backed by recurring consumables revenue, strong margins and increasing global adoption of fluorescence-guided surgery (“FGS”) technologies.

1QFY26 Highlights & Investment Merits

Before diving deeper, readers may refer to my earlier LinkedIn post HERE for a quick overview of ULG’s business segments.

Investment Merits

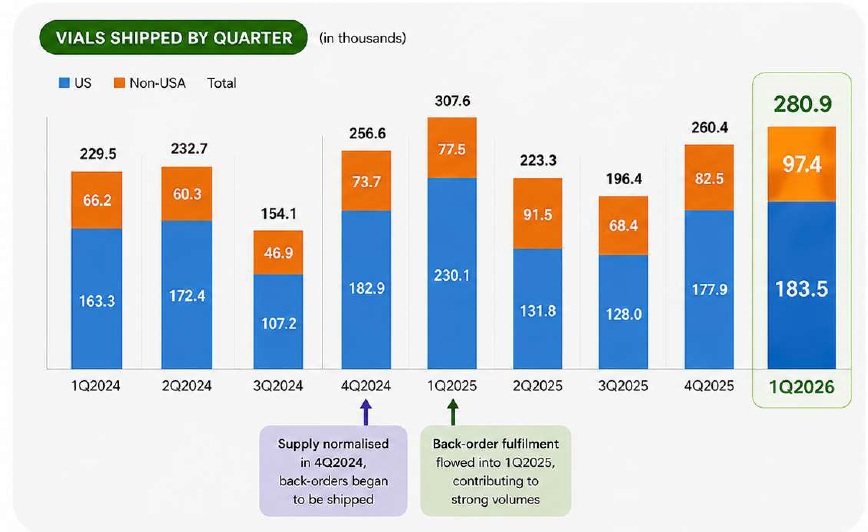

A) Broad-based volume growth across geographies 🌎

1QFY26 shipment volumes improved sequentially across both U.S. and non-U.S. markets, suggesting that underlying demand remains healthy despite difficult year-on-year comparisons due to an exceptionally strong 1QFY25 base.

One interesting observation (see Chart 1 below) is that if we annualise 1QFY26 shipment volumes of 280.9k vials, this translates to approximately 1.1 million vials annually — implying roughly 14% y/y growth.

Importantly, management previously highlighted in its FY2025 annual report that the business generally does not experience significant seasonality due to the recurring nature of demand. This potentially provides investors with greater earnings visibility over time.

Chart 1: Number of vials shipped by quarter (in thousands)

Source: ULG

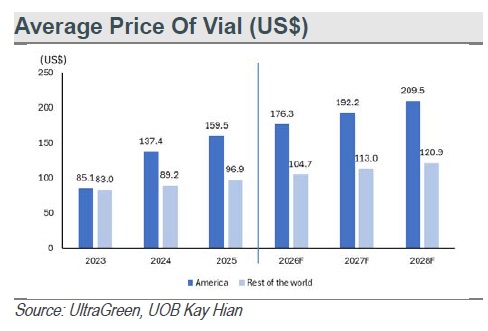

B) Beneficiary of U.S. ASP hikes 💰

Besides volume growth, ULG will benefit from the full-year contribution of average selling price (ASP) increases in the U.S. during FY26.

This is particularly meaningful because:

- The U.S. remains ULG’s largest market.

- ULG commands approximately 83% market share in the U.S. Indocyanine Green (ICG) market.

- Its products appear to face relatively low-price sensitivity due to strong clinical value proposition and rising adoption trends.

Unlike many industries that face persistent pricing pressure, ULG still appears to retain room for further pricing optimisation.

Management also maintained FY26 revenue guidance of US$170m–190m, representing approximately 21%–35% y/y growth.

Chart 2: Average price of Vial – trending nicely higher

C) Structural beneficiary of fluorescence-guided surgery adoption 🔬

FGS adoption continues to expand globally across:

- Colorectal procedures

- Laparoscopic Cholecystectomy

- Breast Reconstruction

- Breast Sentinel Lymph Node

Collectively, these procedures account for more than 10 million surgeries annually. Should even one major procedure become standard-of-care globally, the growth opportunity could become significantly larger over time.

Beyond existing applications, ULG is also exploring additional use-cases such as wound care, potentially opening new long-term growth drivers.

Another underappreciated point is capacity scalability. ULG’s current ICG manufacturing capacity is estimated to be roughly 2x FY26 demand, with potential scalability to 3–5x demand relatively quickly. This positions the company well should demand accelerate meaningfully.

D) Expanding regulatory footprint and international presence 🌏

Verdye is now approved in 41 countries, while ULG’s imaging systems have approvals across 45 markets.

Singapore’s recent approval could potentially serve as a strategic reference point for future ASEAN and Middle East approvals. Management also shared during the 1QFY26 update that approvals are currently being pursued across approximately 20 additional markets in Asia and the Middle East.

If successful, this could further strengthen ULG’s competitive moat and global distribution network over time.

E) Attractive financial profile with strong earnings visibility 📈

Based on Bloomberg consensus estimates, analysts expect ULG to deliver approximately 15% earnings CAGR over the next three years, supported by:

- Rising procedure volumes

- Increasing Asia-Pacific penetration

- Strong pricing power

- Recurring consumables revenue model

What stands out most is ULG’s exceptionally strong profitability profile. According to UOB Kay Hian estimates:

- FY26F Gross Profit Margin (GPM): ~85%

- FY26F Net Profit Margin (NPM): ~48%

These metrics are significantly above broader healthcare industry averages of around (GPM 70%) and (NPM 21%) respectively, highlighting the strength of its business model and operating leverage potential.

Unlike other cash burning pharma companies, ULG ended FY25 with a strong net cash position of approximately US$176m.

F) Analysts are positive with consensus target price US$1.98 (~58% potential capital upside)

Despite its market leadership position and superior margins, ULG still trades at a valuation discount relative to certain comparable healthcare technology peers.

Based on Bloomberg consensus estimates as of 13 May 2026 (see Figure 1 below), analysts have a consensus target price of US$1.98, implying approximately 58% potential upside from the current US$1.25 level.

Continued execution, additional regulatory approvals and stronger market visibility could potentially support further valuation re-rating over time.

Figure 1: Analyst target prices; Consensus TP: US$1.98 (~58% potential capital upside)

Source: Bloomberg as of 18 May 2026

G) Potential dividend policy announcement in 1HFY26 💵

Based on management’s response to shareholders (click HERE), the company expects to communicate its approach towards dividends in 1H2026 after obtaining greater clarity on investment requirements and balancing growth opportunities with shareholder returns.

Should a formal dividend framework be introduced, this could potentially improve investor confidence and broaden institutional appeal.

Key Risks Investors Should Monitor ⚠️

While the long-term growth story remains promising, investors should continue monitoring several key risks closely:

Below are just examples of some risks. Readers can refer to analyst reports HERE to better appreciate the risks.

a) Slower-than-expected FGS adoption

Commercial adoption of FGS technologies in underpenetrated markets may take longer than expected, particularly if hospitals delay capex spending or physician adoption rates soften.

b) Manufacturing and supply chain execution risks

Any delays in expanding manufacturing capacity, supplier diversification or operational scaling could affect ULG’s ability to meet future demand growth efficiently.

c) Competitive and technological risks

Healthcare technology remains a fast-evolving industry. Execution risks relating to AI-enabled products, imaging platforms or future competitive technologies could impact growth expectations.

d) Regulatory risks

Healthcare products remain heavily dependent on regulatory approvals across jurisdictions. Any changes in regulatory approvals may affect adoption momentum.

e) Valuation volatility

Although analysts remain positive, growth stocks — especially healthcare technology counters — can experience elevated volatility during periods of market uncertainty, earnings misses or sector rotation. Investors should therefore expect potentially sharp share price swings.

Conclusion

In summary, ULG continues to benefit from:

- Growing global FGS adoption

- Strong pricing power

- Expanding regulatory approvals

- High recurring consumables revenue

- Attractive profitability metrics

- Significant balance sheet strength

If precision and fluorescence-guided surgery adoption continues to accelerate globally, ULG could remain one of the key long-term beneficiaries within this niche healthcare technology segment.

Despite recent share price weakness, ULG’s latest business update does not appear to suggest that its broader structural growth story has derailed.

That said, investors should continue balancing the company’s attractive growth potential against execution, regulatory and adoption risks.

As always, investors should conduct their own due diligence and consider their own investment objectives, financial situation and risk tolerance before making any investment decision.

Disclaimer

This article is meant purely for general informational and educational purposes and should not be construed as financial advice or a recommendation to buy or sell any securities.

Every investor’s financial situation, investment objectives and risk appetite are different. Please conduct your own due diligence or consult a licensed financial adviser, if necessary, before making any investment decision.

If you’d like to stay updated on my future write-ups or insights, you can sign up at http://ernest15percent.com. There may be a slight delay in emails, as more detailed updates and information are usually shared with my clients first. For example, I have shared Oiltek, OKP and Nanofilm to my clients when they were trading around $0.700, $0.640 and $0.580 respectively last month. Prices move up too fast to have time to do a formal write-up on my blog. 😛

For those interested in working together, feel free to reach out at crclk@yahoo.com.sg.

P.S: I am vested in ULG.

Please refer to the disclaimer HERE