Skylink: One Vehicle, Multiple Income Streams – An Under-The-Radar SGX Growth Story? (10 May 26)

Dear all

Last month, Skylink reported three notable developments — a positive business update (7 Apr), management share purchases (9 Apr) and a positive profit guidance (23 Apr).

Interestingly, despite these developments, Skylink’s share price performance has lagged the broader FTSE ST Catalist Index. Since 7 Apr, the FTSE ST Catalist Index gained 11.2%, while Skylink rose 10.6%.

At first glance, this may not seem significant. However, considering the positive operational momentum and improving outlook, there could potentially be a disconnect between fundamentals and share price performance.

If Skylink delivers a strong FY26 result in end-May together with a constructive outlook, it may simply be a matter of time before the market starts to pay closer attention — especially against the backdrop of a buoyant equity market and improving sentiment towards smaller-cap growth names.

So what exactly is Skylink, and why are some investors starting to take notice?

Let’s take a closer look.

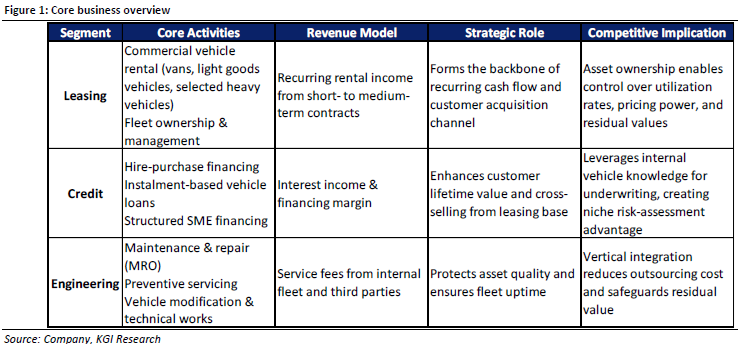

1) Skylink – Various business segments at a glance

With reference to Figure 1 below, Skylink is not just a vehicle rental company. It operates an integrated commercial vehicle ecosystem across three key business segments: leasing, credit and engineering services. These businesses support one another and create recurring income streams across the entire vehicle lifecycle.

2) Investment Merits

A) Various business segments complement one another and add resiliency

Skylink’s leasing business acts as the “customer acquisition engine”, enabling cross-sell financing and maintenance services opportunities.

Skylink’s hire purchase financing for commercial vehicles, besides earning interest income and financing margin, also benefits from its understanding of vehicle conditions and customer behaviour. As it already leases and services many of these vehicles, it arguably has better visibility into customer repayment ability and asset quality compared to standalone lenders.

This segment helps protect vehicle uptime and residual values while lowering outsourcing costs. As the fleet expands, maintenance demand also rises. Furthermore, this segment allows Skylink to understand vehicle conditions better.

In summary,

The key attraction is that Skylink monetises the same vehicle multiple times:

- Leasing income

- Financing income

- Maintenance/service income

- Eventual resale/disposal value

Even if one segment weakens temporarily, the other segments may help cushion earnings volatility. Leasing income tends to be recurring while servicing demand continues as long as vehicles remain operational. This creates a more resilient and diversified earnings structure compared to a pure leasing company.

B) Integrated Business Model Creates Competitive Advantage

Skylink controls the vehicle lifecycle from procurement to servicing and eventual disposal.

This allows the company to:

- Better preserve residual values

- Improve fleet utilisation

- Reduce value leakage

- Potentially enhance long-term ROE

Unlike fragmented competitors, Skylink’s ecosystem increases customer stickiness as clients can obtain leasing, financing and servicing under one platform.

C) Beneficiary of Singapore’s Infrastructure & SME Activity

Singapore’s construction, logistics and SME sectors remain supportive for commercial vehicle demand. Based on The Building and Construction Authority (BCA) statistics, BCA estimates total construction demand of S$47–53b in 2026 and S$39-46b between 2027 – 2030.

Suffice to say that Skylink’s fleet utilisation should benefit as the capex intensive pipeline translates into ongoing on-the-ground works and subcontractor activity, even if the headline GDP growth rate moderates.

D) EV Transition Could Be A Structural Tailwind

Singapore’s push towards commercial EV adoption has already benefitted Skylink. Singapore’s electric heavy vehicles incentives started this year with a total of S$40,000 per vehicle and co-funding up to S$30,000 per accompanying charger. In Skylink’s business update (click HERE), Skylink cited

“With strong execution of the EV conversion strategy, the Group has:

- Gained significant traction in enabling green mobility transition for its customers in several essential sectors, which includes logistics, e-commerce, F&B distribution, and environmental services, among others under its expanding commercial EV lease offerings;

- Secured 18 new contracts and transitioned 16 existing customers to EVs with a total deployment of 43 new EV units in the 3-month period ended 31 March 2026 (“4Q2026”); and

- Recently received more customer enquiries with a robust pipeline of leads for its EV lease offerings specifically during 4Q2026 amidst rising diesel prices, while the overall fleet utilisation rate has remained consistently high”

E) Growth Outlook Remains Strong

Based on Skylink’s positive profit alert on 23 Apr (click HERE), they cited the following

- Higher recurring revenues from Commercial Vehicle Leasing segment – following continued expansion of the Group’s income-producing commercial vehicle fleet;

- Higher margin from Credit segment – for its newly added hire purchase financing loan books; and

- Higher revenues from Engineering segment – following expansion of the Group’s technical capabilities, service offerings and a new base of public sector customers.

F) Management purchase signals confidence

On 9 Apr (click HERE for the announcement), Skylink announced that CEO Wesley bought a total of 200K shares on 8 and 9 Apr at an average price of around $0.250. Both Chairman Mr Teh and CFO Leonard bought 100K shares, both at $0.245.

On the surface, the purchase may look small. However, it is noteworthy that Chairman and CEO hold 12.85% and 55.87% post the purchase.

All in, I believe it signals confidence

3) Key Risks

Besides its concentration risk where its activities are solely focused in Singapore, below are examples of some other risks.

A) Funding Cost & Interest Rate Risk

Skylink relies on borrowings to finance fleet growth. Hence a sudden rise in interest rates is likely to have an adverse impact on their financing margins.

B) Fleet Utilisation Risk

Leasing contributes the majority of revenue. In the event of a slowdown in Singapore’s economic activity, or / and construction activity, there may be a negative knock-on effect on Skylink’s vehicle utilisation rate.

C) Regulatory & COE Policy Risk

Singapore’s commercial vehicle market is heavily influenced by COE policies; emissions regulations and EV incentive schemes etc. Changes in these policies could affect fleet acquisition economics and residual values.

D) Execution Risk

Skylink is expanding rapidly in terms of both organic and inorganic growth. Hence, the usual execution risks apply.

4) Conclusion

Skylink is gradually evolving beyond a traditional vehicle leasing company into a more integrated commercial mobility ecosystem player.

What makes the business interesting is how its leasing, financing and engineering segments complement one another, creating multiple recurring income streams from the same vehicle asset. Combined with Singapore’s infrastructure pipeline, logistics demand and the commercial EV transition, Skylink could potentially enjoy several structural tailwinds moving forward.

That said, investors should continue monitoring key risks such as interest rates, fleet utilisation trends, regulatory changes and execution risks associated with rapid expansion.

As always, investors should conduct their own due diligence and consider their own investment objectives, risk appetite and financial situation before making any investment decision.

Disclaimer

As always, every investor’s situation is different. It’s important to consider your own risk appetite, portfolio exposure, and investment timeframe before taking any action. This article is meant for general informational purposes only. If you require advice specific to your circumstances, do consider speaking with your financial advisor or banker.

If you’d like to stay updated on my future write-ups or insights, you can sign up at http://ernest15percent.com. There may be a slight delay in emails, as more detailed updates and information are usually shared with my clients first. For example, I have shared Oiltek, OKP and Nanofilm to my clients when they were trading around $0.700, $0.640 and $0.580 respectively last month. Prices move up too fast to have time to do a formal write-up on my blog. 😛

For those interested in working together, feel free to reach out at ernestlim15@gmail.com.

Please refer to the disclaimer HERE