Comfort Delgro – Potential bullish morning doji star formation (4 Aug 25)

While screening through the SGX universe, Comfort Delgro is among the rare companies which has all buy recommendations from the analysts.

This article is a brief version of what I have sent out to my clients on 1 Aug and 4 Aug.

Comfort Delgro closed $1.52 on 4 Aug. Day range $1.50 -1.54.

What’s so interesting on Comfort Delgro?

a One of the remaining rare quality mid-cap laggards after the recent blistering rally

FTSE ST Mid Cap Index (FSTM) is a market capitalisation weighted index that tracks the performance of the next top 50 Companies (after the STI constituents) listed on SGX. Comfort Delgro is in this index. Since 9 Apr 2025, FSTM has risen 21% from an intraday low of 565 to 684 on 4 Aug 2025, vis-à-vis STI 25% rally.

Comfort Delgro has only risen 12% from $1.36 to close $1.52 over the same period. In other words, FSTM has lagged STI and Comfort Delgro has lagged FSTM, which makes Comfort Delgro a real laggard.

b Trades at 13.8x FY25E P/E; 5.6% FY25F yield with FY26F dividend yield ~6.1%

Based on Bloomberg, Comfort Delgro trades at an undemanding 13.8x FY25F PE; 5.6% FY25F yield. FY26F dividend yield may reach around 6.1%. Furthermore, it trades at approximately 0.5x standard deviations below both its 10Y PE and 10Y P/BV. Valuations do not seem demanding.

c Possibility of sequential profit growth

Based on Maybank report dated 25 Jul 2025 (click HERE for the full report), they expect Comfort Delgro to post core net profit attributable to equity holders of around S$58m (+10% YoY, +20% QoQ). This is attributable to its various acquisitions such as Addison Lee; EBIT margin improvement in UK bus contract renewals etc.

d Interim dividends potentially ranging from S$0.035 – 0.039 / share

1HFY24 gave out S$0.0352 / share. Maybank expects Comfort Delgro to declare an interim DPS of about 3.9 SG cents this time. If it materialises, it should be positive too.

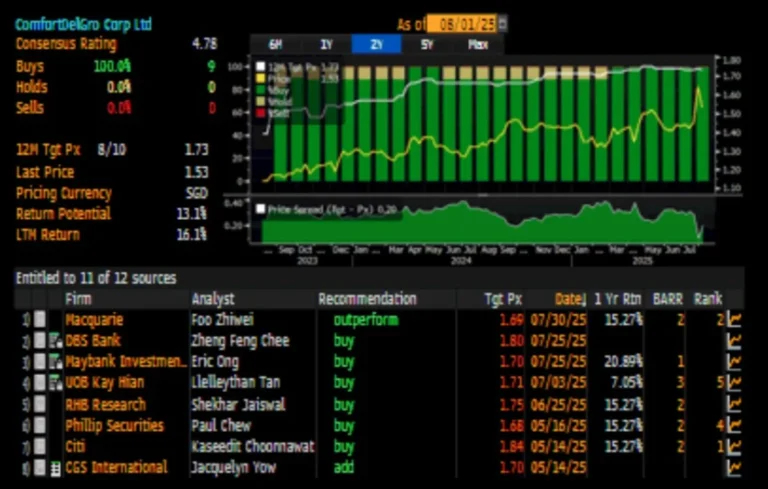

e Analysts are positive in Comfort Delgro with average target price at $1.73

Based on Fig 1 below, out of the eight analyst target prices over the last three months, all have BUY calls on Comfort Delgro with an average target price $1.73. Total potential return is around 19.4%. Given the PE multiple expansion and the robust market sentiment in the market, there may even be scope for analysts to raise target price on Comfort Delgro post 1H FY25 results, if Comfort Delgro delivers.

Fig 1: Average analyst target price $1.73; total potential upside of around 19%

f Chart looks interesting, supported at $1.48 – 1.52

Based on Chart 1 below, Comfort Delgro has retraced approximately 50% of its rally from $1.40 – 1.64. It is now at a confluence of key support region $1.48 – 1.52 where $1.52 is both a 50% Fibonacci retracement level and a resistance turned support level. 14D RSI has pulled back from its multi-year high of 88.6 on 25 Jul to close 54.8. Moreover, Comfort Delgro has halted its decline today, its first out of the past six trading sessions. On the chart, a potential bullish morning doji star formation seems to be in the making. However, we require a price confirmation in the next few trading days for this bullish pattern to be valid.

All in, I view this as a healthy retracement to set the stage for the next up-move.

Chart 1: Potential bullish morning doji star formation

g A Key Beneficiary of MAS-led SGD 5B Equity Market Development Program

Besides the above points, Comfort Delgro is arguably one of the rare non STI component stocks, big and liquid enough, with visible, diversified and resilient operations, strong track record, and good dividends. Hence it is likely to be one of the key beneficiaries of MAS-led SGD 5B Equity Market Development Program.

Potential risks / challenges

Below are examples of some risks only. To better appreciate the potential risks in Comfort Delgro, you can refer to the analyst reports HERE.

a) A decrease in taxi utilisation rate may adversely affect Comfort Delgro.

b) Comfort Delgro may face higher-than-expected operating costs due to on-going inflationary pressures.

c) A decline in ridership for its public transport services may not bode well for Comfort Delgro.

Conclusion

Comfort Delgro lags both the FSTM and STI in terms of price performance. Valuations remain undemanding as it trades 0.5x standard deviations below both its 10Y PE and 10Y P/BV.

Based on Bloomberg, all eight analysts who cover Comfort Delgro rate it a “Buy” with an average target price $1.73. Together with FY25F dividend yield of around 5.6%, total potential return is around 19%.

Usual risks that Comfort Delgro may face include but not limited to a decrease in taxi utilisation; a decline in ridership for its public transport services and higher than expected operating costs etc.

P.S: I have informed my clients to take a look at Comfort Delgro over the past two days. I am vested.

Disclaimer

Please refer to the disclaimer HERE.