Dear all,

This write-up was reproduced in entirety with permission from William Chen, a Senior Associate Marketing Director with PropNex. Please refer to the end of the article for more information on William.

𝘞𝘪𝘭𝘭 𝘱𝘳𝘪𝘤𝘦𝘴 𝘥𝘳𝘰𝘱? 𝘈 𝘵𝘩𝘰𝘳𝘰𝘶𝘨𝘩 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘩𝘦𝘳𝘦…

Many real estate watchers got a surprise when MND announced a new set of cooling measures for residential properties just a few days before Christmas. And I start to receive many questions from my clients who are wondering if prices will drop after this announcement. So I’m going to lay out the facts and figures here, and you can decide for yourself what’s likely to happen over the next few months.

𝟮𝟬𝟭𝟴 𝗰𝗼𝗼𝗹𝗶𝗻𝗴 𝗺𝗲𝗮𝘀𝘂𝗿𝗲𝘀

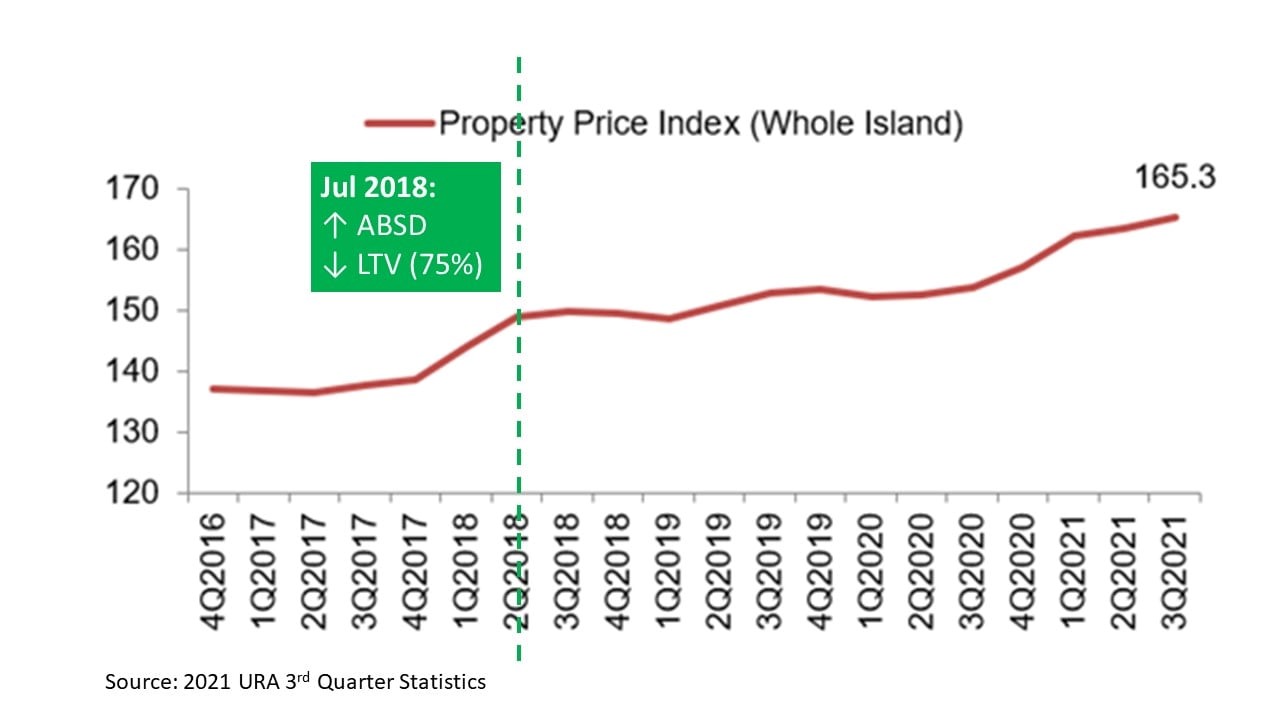

Let’s take a leaf out of a page in history and observe what happened in July 2018. Back then, the government increased ABSD for 2nd/3rd properties and foreigners, and LTV dropped from 80% to 75%. Many buyers felt that prices will drop after that and decided to wait for prices to drop. Taking reference from the URA property price index, prices did correct to a very small extent but those who waited for a significant drop eventually had to pay much higher prices as the market continued to climb. To put things in context, 2018 was the year when Park Colonial launched at around $1700psf, and Stirling Residences launched at around $1800psf. Today, prices have increased to around $2000psf for both developments.

𝗔𝗕𝗦𝗗 𝗶𝗻𝗰𝗿𝗲𝗮𝘀𝗲 𝗶𝗻 𝟮𝟬𝟮𝟭

This time round in 2021, the measures also targeted 2nd/3rd properties, foreigners and companies. Based on my personal and colleagues’ experience, most buyers who buy 2nd/3rd properties would have already decoupled by then, so the impact of this increase is negligible. I’ll explain why… Ever since 2018, buyers who buy 2nd/3rd properties under their same name are already extremely rare. To put things in context, if you had an existing property and an outstanding housing loan, you would need 55% downpayment + min 3% BSD + 12% ABSD for your next property. That means to purchase a $1m condo, you would need at least $700k upfront. How many buyers today are willing or able to do so? Hence, even if ABSD for 2nd/3rd properties increase to 100%, it’s not really going to move the needle much.

𝗧𝗗𝗦𝗥 𝗿𝗲𝗱𝘂𝗰𝘁𝗶𝗼𝗻

Will reduction of TDSR from 60% to 55% make a material impact? That depends on how many buyers previously max out their TDSR when buying properties. Based on personal experience, this is also pretty rare. To put things in context, after the new measures, a household with combined income of $10k taking 30y loan can borrow up to around $1.2m, which translates into a purchase price of about $1.6m. Even taking into account $1,000 of monthly instalments for other loans such as car loans, their max loan would be around $1m, which translates into a purchase price of about $1.33m. This price point would cover at least 70% of 3br resale condos in OCR. With that, it doesn’t seem like the latest TDSR will cause major affordability issues.

𝗘𝗳𝗳𝗲𝗰𝘁 𝗼𝗻 𝗛𝗗𝗕

LTV for HDB loans were reduced from 90% to 85%. Firstly, to qualify for HDB loan, the household income must be below 14k. Secondly, if you are taking HDB loan for 2nd time, you will need to use 50% of your cash proceeds towards the purchase of the next HDB. As such, this measure will impact 1st time buyers more, typically the younger and/or lower income ones who don’t have much cash/CPF and may struggle with the additional 5% downpayment. I don’t understand why the government decided to target this group. Did they see a higher HDB loan default rate from such buyers? On a bigger picture, the overleveraging risk is already addressed by MSR where the max loan will capped based on the buyers’ age and salary. LTV is more relevant to creditors which allows them to recoup their losses in the event of default. So why bother reducing the LTV to 85% with a strict MSR in place? Sorry, I’ve digressed..

Let’s review some numbers here.. If we’re looking at young 1st time buyers, they are likely to explore a relatively new 4 room flat in Punggol which costs around 550k. A 5% reduction in LTV translates into $27,500. Divided by 2 pax, it would be about $13,750 per person. Sounds manageable? Probably… But if the buyers are very young (early 20s) and/or have low income, this would be a huge sum to them on top of any COV that they need to pay. So we might see some impact on younger 3 and 4 room flats which are the typical ones that 1st timers look out for.

𝗘𝗳𝗳𝗲𝗰𝘁 𝗼𝗻 𝗙𝗼𝗿𝗲𝗶𝗴𝗻𝗲𝗿𝘀

With the ABSD increase to 30% from 20% for foreigners, they will obviously reconsider investing in other countries with friendlier tax regimes. Since 2018, ABSD for foreigners was already a punitive 20%, and most working class foreigners would rather rent until they get their PR before buying. As such, most of the foreigner purchases are made by high net worth individuals who tend to buy bigger luxury properties in the Orchard/Marina vicinity. Examples of such properties are South Beach Residences, Boulevard 88 and Park Nova. Sales of such properties will likely suffer the biggest impact. OCR/RCR properties don’t have much foreigner interest in the first place ever since 2018, so even if ABSD for foreigners increase to 100%, it won’t really affect this segment.

𝗣𝘂𝗹𝗹𝗯𝗮𝗰𝗸 𝗳𝗼𝗿 𝗘𝗻𝗯𝗹𝗼𝗰

The biggest losers from these cooling measures are likely owners of properties who are looking forward to enbloc (e.g. Mandarin Gardens, International Plaza, etc). With the latest measures, if developers are unable to sell all their units within 5 years, they will need to pay 40% ABSD (up from 30%) of the purchase price. To put things in context, the average profit margin for developers now are around 15-20%. If you are a developer acquiring properties for enbloc redevelopment, are you likely to adjust your bid price to account for the increase in risk? Of course! Especially for such a huge site like Mandarin Gardens, the risk of selling everything within 5 years is substantially higher. Against the backdrop of weaker buying sentiments from the latest cooling measures, developers are not likely to offer a good price for the enbloc. The first group of could-have-been enbloc beneficiaries that got extremely disappointed was the owners at High Point (a condo at district 9), whose enbloc sale was aborted by Shun Tak after giving up a $1m tender deposit.

But here’s a contrarian view. If enbloc transactions don’t go ahead because of mismatch in expectations between owners and developers, new private property supply will continue to remain low over the next few years compared to the number of new launches in 2018-2020 which was the result of the enbloc fever in 2017-2018. What do you think how that will affect prices in the medium to long run?

𝗖𝗼𝗻𝗰𝗹𝘂𝘀𝗶𝗼𝗻

Transactions will inevitably slow down as a knee jerk reaction to this unwelcomed Christmas gift from MND. However, other than HDB flats that are mostly sought after by 1st time home-buyers, the impact for own-stay properties will be minimal as there is hardly any ABSD or TDSR impact on buyers and sellers. Luxury segment will suffer a slow down in transactions, and enbloc owners will need to be more realistic in their asking prices for developers to bite. Otherwise, the new supply of properties will struggle to catch up with population growth which will accelerate after borders reopen. When that happens, do you think prices will go up or down? You decide!

About the Author

William empowers his clients to make informed real estate decisions by using objective facts and figures to identify market trends, and more importantly, make price forecast for different types of real estate. Prior to joining Real Estate, he was a senior banker for over 10 years, covering regional responsibilities across 19 countries in Asia Pacific. Since then, he has helped many clients transit seamlessly into their new properties and/or make profitable investments in their real estate portfolio. Do follow his Facebook page in the link below for more real estate related posts and independent client reviews.

https://www.facebook.com/PowerhausSG

Disclaimer

Please refer to the disclaimer HERE

هودی تدی در ظاهر به دلیل کرک دار بودن شبیه خز است؛ ولی پرزهای

کوچک تر و کوتاه تری دارد. به همین دلیل می توان این نوع سویشرت

را در دسته هودی پشمی پسرانه به حساب آورد.

جستجوی پیشرفته پاک کردن فیلترها

فقط کالاهای موجود بله قیمت

Thank you, I’ve just been looking for info about this topic for a

while and yours is the greatest I have discovered

so far. However, what concerning the bottom line?

Are you certain about the source?

I’m extremely impressed with your writing skills and also with the layout on your weblog.

Is this a paid theme or did you modify it yourself?

Anyway keep up the nice quality writing, it’s

rare to see a nice blog like this one nowadays.

Link exchange is nothing else except it is simply placing the other person’s web site

link on your page at suitable place and other person will also do similar for you.

Thanks for the article post.Really looking forward to read more.

طرح و رنگ این هودیها باعث شده تا بسیاری از آقایان خوش تیپ و جذاب، طرفدار این

لباس شوند. از آن جایی که کیفیت لباس یکی

از مهمترین مواردی است که باید در نظر داشته باشید، برای خرید

هودی ارزان و باکفیت میتوانید از طریق فروشگاه اینترنتی

پارچی اقدام کنید.

بنابراین خرید سوییشرت و هودی دخترانه یک خرید ترندی خواهد بود.

It is appropriate time to make some plans for the future and it is

time to be happy. I have read this post and if I could I wish to

suggest you few interesting things or advice. Perhaps you could write next articles referring to this article.

I want to read more things about it!

Hello there! This is kind of off topic but I need some advice

from an established blog. Is it very difficult to set up your own blog?

I’m not very techincal but I can figure things out pretty

fast. I’m thinking about setting up my own but I’m not sure where to

start. Do you have any tips or suggestions? Thank you

Quality content is the secret to attract the users to pay a

visit the website, that’s what this web page is providing.

Appreciation to my father who shared with me concerning this

web site, this web site is truly amazing.

It’s enormous that you are getting thoughts from this piece of writing as well as from our dialogue made at this place.

I used to be able to find good info from your content.

Have you ever thought about adding a little bit more than just your articles?

I mean, what you say is valuable and everything. But think of

if you added some great pictures or video clips to give your posts more, “pop”!

Your content is excellent but with pics and videos, this blog could certainly be one

of the most beneficial in its niche. Amazing blog!

If you want to grow your know-how simply keep visiting this web site and

be updated with the newest news update posted here.

I’m not sure exactly why but this website is loading

incredibly slow for me. Is anyone else having this issue

or is it a problem on my end? I’ll check back later and see if the problem still

exists.