Dear all,

I have been doing my regular market analysis (homework) and after reading many pessimistic or “not so good” reports, I decided it is an opportune time to do a short write-up on our Singapore market.

Recent sell off in the equity markets due to

The recent sell off may be attributable to the following reasons

a) Exodus of funds from equity markets

Based on Figure 1 below, U.S. funds saw the largest weekly outflows amounting to US$12.3b, the largest since 2000. The Asia funds suffered US$4.9b of weekly outflows.

Figure 1: Exodus of funds

b) Technical breakdown in the charts

STI has traded within a tight range of approximately 130 points from 2 Jun 2015 to 21 Jul 2015, before it broke down. Coupled with the simultaneous breakdown in the other equity markets’ charts such as S&P500, Hang Seng, China, there was widespread risk aversion.

c) 2Q GDP sparks concerns of a possible technical recession

Singapore 2Q GDP contracts by 4% q/q, sparking concern of a technical recession if 3Q GDP continues to be negative on a q/q basis. Furthermore, our strengthening SGD against the other ASEAN countries’ currencies and China’s Yuan, reduces our competitive nature.

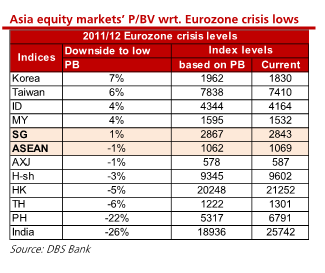

Notwithstanding the above factors, Singapore market (as measured by our STI) has fallen around 15% year to date and is likely to be in the process of probing for a bottom. With the recent slide, STI trades at around 1.1x Price to Book Value (“P/BV”) which is on par with that during the Eurozone Crisis. This should provide some downside support to the market in the event of further weakness.

Table 1: Asia equity markets’ P/BV valuations vs Eurozone crisis lows

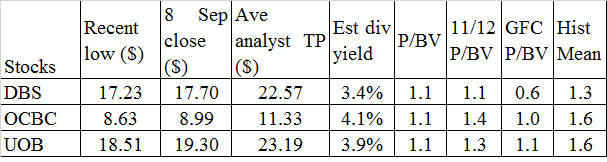

In the STI, our three local banks are trading at depressed valuations amid concerns of slower economic growth in Singapore and possibility of rising non-performing loans etc. In addition, according to DBS, as overseas earnings comprise of 1/3 of our local banks’ pre-tax earnings, exposure to HK/China, Indonesia and Malaysia also raise their risk profile.

Notwithstanding the cautious outlook on the three local banks, their recent share price weakness has brought valuations to depressed levels, especially for UOB and OCBC. Both UOB and OCBC are trading near the global financial crisis (“GFC”) lows (See Table 2). It is noteworthy that OCBC and UOB mostly trade above DBS in terms of P/BV valuation since 2002.

Table 2: Banks’ P/BV valuations vs their historical means

Source: Bloomberg; Philips Securities

In times of capitulation, it is entirely possible that the banks may trade at valuations even lower than GFC lows. What we know for now (based on statistics) is that, the banks are likely trading at levels nearer to the lower end of their historical valuation bands. When sentiment recovers (be it in the coming months or years), it is likely that the local banks may re-rate nearer to their historical means.

In addition, it is unlikely that the slowdown or / and turmoil in the China market are serious enough to bring a global recession as to what we have seen in 2008/2009. There remain sufficient supports from cheaper oil, lower bond yields, monetary easing in Emerging Markets and Europe and strength in the U.S. economy.

Conclusion – attractive valuations for long term investors, awaiting re-rating catalysts

Given the recent multitude of concerns ranging from the impending U.S. rate hike, slowing China economy, turmoil in the China markets (etc., the list goes on…), most investors will prefer to stay mostly, or entirely in cash. Such investors typically belong to the following two groups.

Group 1: Investors already have existing exposure to equities and they are not comfortable to add more now based on their risk profile and market outlook.

Group 2: Investors prefer to buy when they are absolutely certain that market has bottomed. This approach is ideal if

a) Investors can pick the absolute bottom on a consistent basis AND

b) In the event that they miss the absolute bottom, they are ready and fast to buy stocks when the stocks are on the way up.

However, most people (including me) are not able to pick the absolute bottom on a consistent basis. My personal view is that investors with a long term basis should consider accumulating blue chips with good dividends (e.g. banks) via tranches. We can collect dividends while waiting for the stocks to re rate closer to their historical valuations.

Lastly, I have just sent my clients my personal compilation of stocks whose past year P/BV are lower than their average five year P/BV (i.e. stocks are cheaper now than their five year historical average) together with this write-up. I will forward my list to the readers on my http://ernest15percent.com/ website signups in the next couple of days.

Disclaimer

Please refer to the disclaimer here http://ernest15percent.com/index.php/disclaimer/ .

Goood article. I certainly lve tjis site. Contonue the goood

work!

can i order cytotec without prescription VERAPAMIL EXTENDED RELEASE ORAL

Oliguria is when you pee less than usual where can i buy generic cytotec pill

you will have to wait for results first to see where are u with your pregnancy where to buy propecia from the states

супрастин инструкция по применению таблетки https://allergiano.ru/ .

Play on 888Starz Casino and maximize your rewards with 888LEGAL.