Dear all,

Marco Polo Marine (MPM) has caught my attention.

It closed at $0.055 on 5 Feb 2025.

Read on as I outline the reasons that it has caught my eye.

Firstly, what does MPM do?

MPM, listed on the SGX-ST since 2007, is a regional integrated marine logistics company involved in shipping and shipyard operations. The company charters offshore support vessels (OSVs) and tugboats/barges for industries such as mining, construction, and infrastructure across regional waters, including the Gulf of Thailand, Malaysia, Indonesia, and Taiwan. It has expanded into offshore wind farm projects, capitalizing on the growing wind energy industry in Asia. Additionally, the company operates a shipyard in Batam, Indonesia, offering shipbuilding, repair, and maintenance services, with three dry docks and a 34-hectare site. A fourth dry dock is expected to come on stream and commence contribution in 1HFY25F.

Some interesting points which attract me to MPM

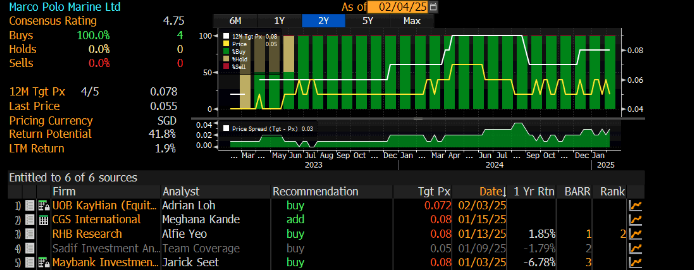

a) Analysts are generally positive with average target price $0.078

With reference to Figure 1 below, four analysts cover MPM and all rate it a “Buy”. Average analyst target price is $0.078 with potential capital upside of around 42%.

In fact, UOB KH also has an oil and gas report out dated 3 Feb 2025 where they cite Seatrium and MPM as their top picks. Click HERE for the report.

Figure 1: Consensus target price $0.078, potential capital upside of around 42%

Source: Blmberg 4 Feb 2025

b) CSOV – on track to commence work with Vestas from Mar 2025 onwards

MPM expects to showcase its commissioning service operating vessel (CSOV) at their Batam shipyard on 12 Feb 2025 (see pt c below). This is an accommodation support vessel for technicians (akin to a floating hotel) during maintenance and operations. It can house 110 men.

Recall that this CSOV is expected to commence contribution to MPM’s results in 2QFY25F with progressive contributions over time (as issues may crop arise in the first 6-8 months of operation) and significant contribution in FY26F. Based on analyst reports and my interaction with management, average day rates for CSOV are around US$45,000 – 50,000 / day. Average utilisation for their CSOV is likely to be near 95% in the first two years of operation.

c) Large scale site visit on 12 Feb to show case their CSOV

MPM is hosting a large scale one day tour at their Batam shipyard to showcase their operations and their CSOV. Based on grapevine, there may be as many as 50 analysts, fund managers, shareholders etc. are likely to attend.

d) Sound balance sheet with net cash of S$35.8m

Their industry is rather capital intensive. It is rather assuring to see that MPM has a strong balance sheet with net cash amounting to S$35.8m as of end Sep 2024, translating to around S$0.009 / share. This net cash comprises of 16% of MPM’s market capitalisation. MPM’s NAV / share is around $0.054 / share.

e) Stars are falling in place for MPM

For MPM, stars are falling in place.

Firstly, MPM expects to add two more crew transfer vessels (CTVs) in FY25F, bringing the total to five. Based on CGSI report dated 15 Jan 2025, CGSI estimates that each CTV can contribute approximately US$2.0m in revenue in Taiwan. If this CTV operates in Korea, it may fetch 70% higher in terms of revenue as charter rates are higher in Korea.

Secondly, according to Clarkson, the general charter rates for anchor handling tug supply vessels (AHTs) and platform support vessels (PSVs) have risen 2-16% y-o-y. MPM has 8 tugboats and 6 barges with vessel age 6 – 15 years.

Thirdly, as some of you may have read, with the reopening of the Chinese shipyards, this leads to lower repair volumes for other shipyards. MPM was initially affected but demand for their ship repair services has since returned to normal. In FY2024, the average utilisation of their docks for ship repair was 91% compared to 84% in FY2023. It is also noteworthy that in FY24, one of the three docks was allocated exclusively to the CSOV construction from May to August 2024, effectively reducing the Group’s capacity for revenue-generating ship repair projects. With the completion of its CSOV, this frees up space in that dry dock. As of Sep 2024, all three dry docks were available for ship repair activities.

Fourthly, MPM is building a fourth dry dock which is estimated to complete in Feb 2025. This may increase its capacity by up to 25% to boost revenue.

Perhaps in view of the above, management has bought in after MPM posted its FY24 results (see Point f below).

f) MPM’s key shareholders bought in around $0.053 in early Dec, and $0.055 this month

After MPM’s FY24 results announcement on 28 Nov 2024, it is encouraging to see some insiders acquire MPM’s shares in the open market.

On 2 Dec 2024, Mr Darren Teo bought 800K MPM shares at $0.052 which brought his total stake in MPM to 614.4m shares (16.4% of the issued share capital). Furthermore, on 4 Feb 2025, Darren bought another 500K MPM shares at $0.055. This raises his stake to 614.9m shares.

On 4 Dec 2024, Mr Sean Lee acquired 2.0m MPM shares at $0.053, raising his total stake in MPM to 179.2m shares (4.8% of the issued share capital)

g) Dividend and 1QFY25F around the corner

MPM will ex div $0.001 / share on 14 Feb 2025. It will have its 1QFY25F results briefing on 19 Feb.

Risks

Naturally, there are (almost) always risks in stock investing.

Examples of some risks are

- CSOV – As it is their first time operating their new CSOV, there may be hiccups. However, this should be alleviated over time.

- Delays / Cancellations in offshore wind projects affecting vessel demand.

- Difficulty in securing cost-effective financing to acquire vessels.

- Drop in oil prices hitting sentiment and charter rates.

- MPM’s 1H is seasonally weaker than 2H. Although quarterly results may be difficult to predict, it is likely that MPM’s FY25F should be stronger than FY24 given the aforementioned factors.

- Serious conflict between China and Taiwan affecting their chartering business.

- Global recession or another Covid like event.

Technical analysis

MPM has traded in a broad range $0.051 – 0.058 for the past three months.

Based on Chart 1 below, it seems to have breached the downtrend line established since 17 May 2024 and is now using the line as a resistance turned support region.

Indicators are mixed with OBV and MACD exhibiting bullish divergences. RSI is forming higher lows, in line with price. My personal view is that MPM should see strong support around $0.052 – 0.054.

Near term supports: $0.054 (50D SMA) / 0.052 (rising trend line, Fibo)

Near term resistances: $0.057 – 0.058 (Fibo, 200D SMA) / 0.060 (Fibo)

Notwithstanding the above, I hasten to add that chart analysis is subjective. Furthermore, it does not take much to move small cap stock regardless of technicals.

Chart 1: MPM seems to have strong support $0.052 – 0.054

Source: TradingView 4 Feb 2025

Conclusion

It is noteworthy that there are risks involved such as the aforementioned risks (e.g., China / Taiwan conflict; drop in oil price affecting sentiment and charter rates etc.). Nevertheless, suffice to say that FY25F is likely to be a better year for MPM, with contributions from various segments.

For a more complete picture, it is advisable to refer to MPM’s analyst reports (Click HERE); SGX website (Click HERE) and MPM’s corporate website (Click HERE). Readers can also refer to the informative Kopi-C interview with MPM’s CEO Sean published on the Edge this evening (Click HERE).

Readers have to assess their own % invested, risk profile, investment horizon and make your own informed decisions. Everybody is different hence you need to understand and assess yourself. The above is for general information only. For specific advice catering to your specific situation, do consult your financial advisor or banker for more information

Readers who wish to be notified of my write-ups and / or informative emails, you can consider signing up at http://ernest15percent.com. However, this reader’s mailing list has a one or two-day lag time as I will (naturally) send information (more information, more emails with more details) to my clients first. For readers who wish to enquire on being my client, I can be reached at ernestlim15@gmail.com.

P.S: I am vested in MPM.

Disclaimer

Please refer to the disclaimer HERE

Preteen sex stories true stories on child sexual abuse

https://open-mouth-facial-famous.fetish-matters.com/?america-ellie

This article grabbed my attention, thought you’d like it too http://moskat.flybb.ru/viewtopic.php?f=2&t=4871

Local amateur porn find local porn made by amateurs near you

https://teacher-shemales.fetish-matters.net/?kayli-alexus

Swallowing amateur porn 146 949 sex videos qqq porn

https://indian-fitness.fetish-matters.net/?bailee-evelin