The sudden Singapore property market cooling measures on 5th July 2018 had shocked the market as no one was expecting this measures. Many panicked causing a knee-jerk reaction which caused developers to launch 3 projects on the very night these measures were announced, find out more about these measures in this article and how it affects you.

In any measure, there will be different impact on different groups of stakeholders. Inadvertently, there are winners, losers and opportunities created.

In this article, four main questions will be discussed

1.How does the cooling measures affect different groups of people?

2.What is likely to happen to a few market segments?

3.What are the side effects?

4.Are there any winners?

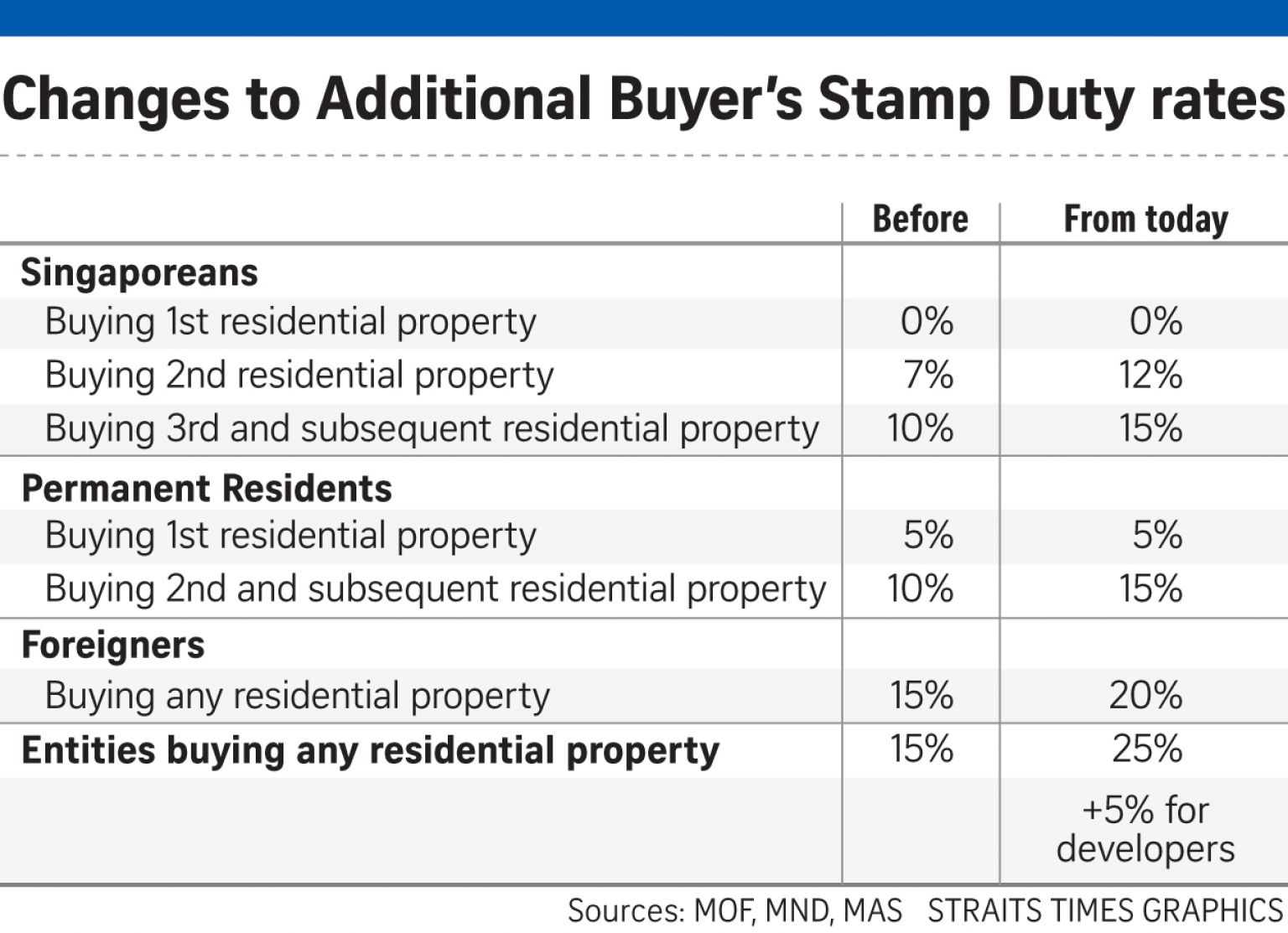

For those who would like to read more about the cooling measures can do so at the appendix attached at the end. As analyst described the latest cooling measures on 5th July 2018 as a tough one, we look to decode the effects of these latest measures.

1.How does the cooling measures affect the following groups of people:

Home owners

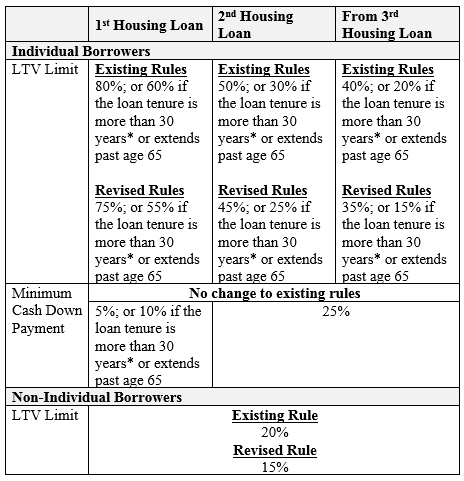

Going forward, home owners will require more cash/CPF for home owners to decouple and buy two properties going forward. With the new 75% LTV ratio instead of 80%, upgrades would need to top up an additional 5% (or $50,000 if the property is $1 million). With two properties and you would need to have $100,000 more in cash/CPF. This extra amount could have been used as an emergency fund. Henceforth, it will be more costly for families who intend to decouple; buy one property for stay and the another for investment. This also means that in order to own two properties, you now need to pay more and loan less, which essentially is more stable for the market. However, home owners who want to cash out their existing property investments, at a higher price, may now face challenges with home staging due to potential decreased affordability by some buyers.

First time home buyers (Singapore Citizen/SPR)

First time home buyers or hdb upgraders are likely to benefit from the latest round of cooling measures if they have the extra 5% cash/CPF (LTV 80% drop to 75%). This is because sc or spr buying their first properties are not impacted by the increase of stamp duty. Property Developers may eventually start to offer some discounts to buyers if the demand start to taper. In line with the government’s intention to keep the property prices stable, home buyers will not have to face runaway home prices. First time buyers who do not have the extra 5% which is about $50k for a $1mil property. Will be priced out of the market. What this would do is to bring back demand to Resale HDBs and BTO Flats, which have a much lower quantum, and therefore require a much lower downpayment.

Second property investors (Singapore Citizen)

Example Calculation for ABSD:

| Total stamp duty payable on or before 5th July 2018 | Total stamp duty payable on or after 6th July 2018 |

| Property Value: $2mil

Buyer Stamp Duty: $64,600 ABSD (7%): $140,000 Total Stamp Duty: $204,600 |

Property Value: $2mil

Buyer Stamp Duty: $64,600 ABSD (12%): $240,000 Total Stamp Duty: $304,600 |

For those buying a second property, with an existing loan, they would need to pay additional 12% Additional Buyer Stamp Duty (ABSD), and can only take a smaller loan of 45% LTV instead of 50% LTV. Consequently, they need to pay a total cash/CPF upfront of 71% (55+4+12) of cash and/CPF to purchase a second property (assuming that there is an outstanding loan), instead of upfront cash/CPF 61% (50+4+7). If there is no existing loan, then financing of up to 75% LTV is possible, and the upfront downpayment required will be cash/CPF 41% (25+4+12), instead of cash/cpf 31% (20+4+7) before the cooling measures were in place.

Third property investors (Singapore Citizen) & Second property investors (SPR)

Example Calculation for ABSD:

| Total stamp duty payable on or before 5th July 2018 | Total stamp duty payable on or after 6th July 2018 |

| Property Value: $1.5mil

Buyer Stamp Duty: $44,600 ABSD (10%): $150,000 Total Stamp Duty: $194,600 |

Property Value: $1.5mil

Buyer Stamp Duty: $44,600 ABSD (15%): $225,000 Total Stamp Duty: $269,600 |

Singaporean Third property investors would only be able to take loan of 35% LTV (if they are taking a third property loan). This means that the upfront cash/CPF is now 84% (65+4+15). For Singapore Citizen third property owners but with a second property loan, or a Singapore PR buying 2nd property and taking 2nd property loan, they would require to have cash/CPF of 74% (55+4+15). For those who are after the third property but taking first property loan, the upfront cash/CPF will be 44% (25+4+15). Clearly, largest impact of the cooling measure is on Singaporeans who intend to buy their third property.

Foreigners

Example Calculation for ABSD:

| Total stamp duty payable on or before 5th July 2018 | Total stamp duty payable on or after 6th July 2018 |

| Property Value: $4mil

Buyer Stamp Duty: $144,600 ABSD (15%): $600,000 Total Stamp Duty: $744,600 |

Property Value: $4mil

Buyer Stamp Duty: $144,600 ABSD (20%): $800,000 Total Stamp Duty: $944,600 |

Foreigners will now need to pay an additional 5% ABSD, which is a total of 20%. In a case study where Foreigners were to buy their first property with the usual 60-70% loan, let us assume that they can take 70% loan, the total downpayment would be 54% (30+24). If it was a $2 million property, the initial cash outlay required would be $1.08 million. The tax that they have to pay on a $2 million property has increased by $100,000. This inadvertently implies that only foreigners who have a real need to own a Singapore property will buy one out of necessity. Furthermore, those who are buying for investment may only consider as a form of portfolio diversification of funds and perhaps due to the stability of Singapore’s currency. Foreigners may consider investing in commercial offices or retail F&B shops as these are not affected by cooling measures.

Developers

Developers will face higher fixed cost with the additional 5% ABSD, which is required to be paid upfront (non-remittable). Developers have been facing rising costs from increased development charges, increased land cost and now the additional ABSD is essentially a further increase in land cost (acquisition costs). In normal circumstances, the Developers will transfer this cost to consumers (property buyers), but with the new cooling measures in place, it may be a challenge to transfer this costs to consumers. Therefore, Developers will have to look to reduce acquisition costs, and pay less for en bloc or land acquisitions in order to lower the launch prices. Hence, there will be a larger impact on the en bloc market which will be discussed in a later section.

2.What is likely to happen to the markets?

Residential Rental Market – this segment is likely to remain stagnant, instead of downtrend. Some foreigners who intended to buy may decide that continuing to rent would be more economical, as they may not want to fork out the extra cash for stamp duty.

Private Residential Sales Market – this segment is likely to remain stagnant as well, and for some areas with lower demand, have a bias to the downside. Overall transaction volumes is expected to drop.

En bloc Market – this niche segment is expected to have lower prices due to the new developer’s additional 5% ABSD, added to the recently increased Buyer Stamp Duty (BSD) for properties above $1 million which affects developers having to pay 1% more tax (4% instead of 3% before). The total additional tax is about 6% (Absd 5% + 1%), subsequently increasing the developer’s fix cost by 6%. If they are unable to pass this extra cost to future buyers (due to cooling measures), they are more likely pay less for en bloc sites and land acquisitions. En bloc sales committees may need to consider a lower reserve price in order to attract Developers.

3.What are the side effects?

Property Developers/Agencies Shares – on the 6th of July 2018, we saw listed property developer stocks/shares drop by about 15% and agencies like ERA (APAC Realty) and PropNex stocks/shares drop by 20%. It is likely that we may see the continuation of a downtrend in public listed property stocks, reminiscent to 2013 when similar cooling measures were intensified.

Capital outflow (flight) – in search for better yield, some investors may consider to invest in good quality assets overseas for their investments or retirement plans. The government had already prepared for this phenomena by getting CEA to come up with certification courses like Marketing Foreign Properties (MFP) to improve knowledge and professionalism of local agents marketing foreign properties so that we can better advise on these investments. In a way, some of us already knew that the recent cooling measures were inevitable and imminent.

4.While it is all doom and gloom, what are the opportunities? Who are the winners?

Private Property sellers who want to cash out will likely price their units at a more reasonable price due to the cooling measures. Therefore, First time condo buyers with sufficient cash/cpf available could take advantage of this situation to negotiate for a better deal. First time buyers without sufficient cash/cpf for the increased downpayment for a condo purchase, may need to reconsider a resale HDB or BTO instead, due to a much lower quantum. This coupled with the potential increased demand in resale HDB flats from the En Bloc owners rightsizing, will in turn, helps to bring back demand for resale HDBs and likely will stabilize the HDB market, possibly mitigating a downtrend. Eventually, these HDB owners may upgrade to their dream condominium at a fair and better price. Selling HDB at a fair price, and buying a condo at a better price. (HDB prices revise upwards and condominium prices stagnant consequently close the gap). This is inline with what the government intends, which is to prevent the widening gap of HDB and condo prices.

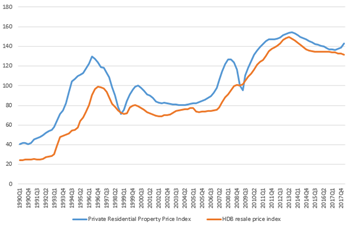

Source: TodayOnline, URA Image: Widening Gap of Private vs HDB prices

Essentially, the cooling measures ensures that only cash rich investors, can make their purchases.

In addition, many property investors in Singapore have focused their attention on the local market. But in fact, there are opportunities to invest in developing countries at low calculated risks. It may be time to learn and research more about these overseas property investments. Stay tuned for more.

Appendix 1-1: Latest Cooling Measures 5th July 2018 (Wef 6th July 2018)

Appendix 1-2: Latest Cooling Measures 5th July 2018 (Wef 6th July 2018)

*This write-up was reproduced with permission from Ray’s Estate Clinic, written by Founder, Raymond Chng.*

About the Author

Ray’s Estate Clinic (REC), founded by the affable Raymond Chng, is a platform for Investors’ and homeowners to have a Property Portfolio Health Check by utilizing data analytics, ensuring that their portfolio remains healthy providing optimized returns.

“Health is Wealth” is what Raymond believes in, and it is not related only to your own body’s health, but it also refers to one’s financial health. Having a Property Portfolio that is not performing does not help improve an investor’s wealth. Hence, converting non-performing assets into optimized performing assets is essential to portfolio’s health improvement.

Raymond graduated with a Bachelors Degree in Business Management (Finance) from the Singapore Management University, and has been in the real estate industry for almost a decade. He believes that marrying financial analysis with real estate data is the future of real estate investment. Having successfully invested in equities, real estate and other asset classes, he works with various domain experts to provide a holistic solution for anyone keen to improve their Property Portfolio Health.

Raymond can be reached at raysestateclinic@gmail.com

Disclaimer

This article, publication or newsletter is purely for educational and entertainment purposes only. Material in this article comes from many sources and may be inaccurate or incomplete. The author does not warrant the completeness, accuracy or timing of any information herein. This is not an offer to buy or sell real estate properties. Information or opinions on this blog are presented solely for educational and entertainment purposes, and is not intended nor should they be construed as investment advice. Under no circumstances shall the authors and its agents, or any third party providers, ever be liable for any direct, indirect, incidental, punitive, special or consequential damages, or any attorney fees, from any person or entity that has viewed this blog. View this article or publication at your own risk. It is advisable that readers seek their own professional advice.

Also, please refer to the disclaimer HERE

Wow, superb blog format! How long have you ever been running a blog for?

you make blogging look easy. The full glance of your

web site is wonderful, let alone the content material!

You can see similar here ecommerce