Golden Energy (“GEAR”) has slumped 21% from $0.655 on 12 Dec 2016 to $0.515 on 27 Mar 2017. Compare this with a 47% rally in Geo Energy’s share price over the same period. Moreover, GEAR has slumped 10% post its results notwithstanding the strong set of results. Why is this so?

I have managed to fix an exclusive 1-1 meetup with Mark Zhou, Head of investments, GEAR (“Management”) to find out more about the company’s business and prospects.

Key takeaways from the meetup

Bullish on FY17F

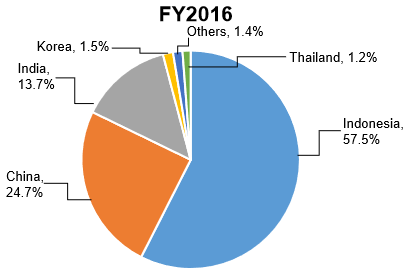

Management continues to be bullish about its outlook. Based on Chart 1 below, Indonesia, China and India contributed about 58%, 25% and 14% respectively. For example, Indonesian government under President Jokowi’s administration has implemented an electrification programme to add 35,000 megawatts (MW) in power generation capacity across the country by 2019. Of which, almost 20,000 MW will come from coal-fired plants. Moreover, there is increasing budget allocated to infrastructure development which fuels demand for cement. Coal is used intensively in the cement manufacturing processing plant.

According to management, China’s coal imports, which has surged 64% to 24.91 MT in January this year, is also projected to increase further as a result of restrictions on local productions and its recent ban on North Korean coal import. However, management does not see any negative spill over effects from China limiting imports of low-quality coal. (See next point)

Power generation in India, which is reliant on coal-fired power to meet soaring domestic energy demand, is expected to increase to around 1,750 TWh by 2020, with coal accounting for more than 1,230 TWh Southeast Asian countries, including Thailand, the Philippines and Vietnam are growth markets for thermal coal in the years out to 2020 as coal-fired electricity is used to fuel their fast-growing economies

All in, the outlook for coal continues to be positive.

Chart 1: Geographical split of GEAR’s revenue

Source: Company

GEAR unaffected by China clamping down on imports of low quality coal

Based on a Reuters’ article this month, China is controlling imports of low-quality coal amid concerns on smog and overcapacity in the world’s top coal consumers. However, management does not see any negative spill over effects. In fact, it is seeing robust demand for their coal which they attribute to its flexibility. This is because due to GEAR’s coal specifications (BIB 4,000 – 4,200 GAR) and large reserves, it can sell to power producers. Furthermore, as their coal has low ash and sulphur content, there is demand for their coal for blending with higher sulphur coal.

Confident of getting regulatory approval to raise BIB mine production from 7.5MT to 12MT

Management plans to ramp up coal production from 9.5MT in FY16 to 14.0MT in FY17F. This comes mainly from the BIB mine which is targeted to increase production from 7.5MT in FY16 to 12MT in FY17F, subject to regulatory approval. GEAR is confident of getting the regulatory approval.

Ramping up investor awareness

For such a large company of S$1.2b, GEAR is only covered by one brokerage house, KGI Securities. KGI ascribed a target price for GEAR at $0.960 with an estimated net profit attributable to shareholders amounting to US$100m, which is almost 5x that of FY16 net profit.

In view of the above, management is cognizant that it can do more to engage the investment community. It is doing a presentation to retail investors at SGX seminar on 30 Mar 2017. Furthermore, it is planning a site visit around the week of 20th Apr 2017 for analysts and media.

Comparison between Geo Energy and GEAR

As Geo Energy is the closest comparable listed on SGX bourse, I have made a simple comparison between the two. Based on Table 1, GEAR seems to be better than Geo Energy as it has a larger market capitalisation, net cash, larger reserves, lower cash cost and lower market capitalisation per ton of reserves.

Table 1: Comparison between Geo Energy and GEAR

Source: Companies’ FY16 results

* Geo Energy reserves include the acquisition of TBR, to be completed in 1H17

** I couldn’t find the cash cost in Geo Energy FY16 results and I used Philip Securities estimate for FY17F

** For GEAR, management believes that the cash cost should broadly stay around the above level in FY17F

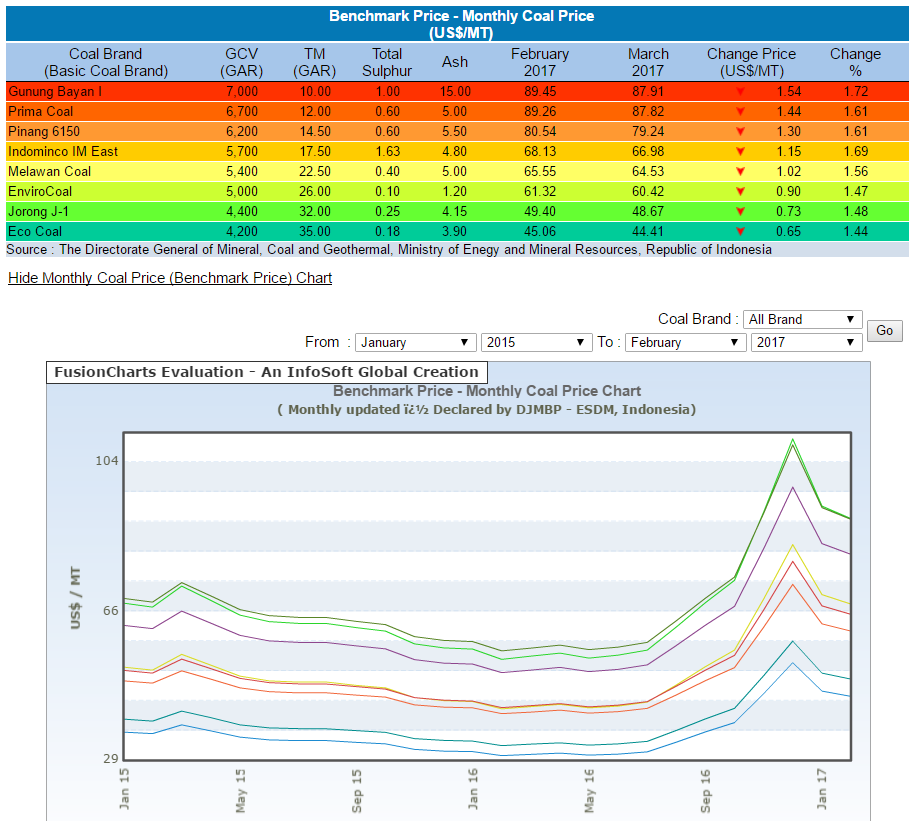

Coal prices may have bottomed last year

Based on Chart 2 below, although coal prices may have hit a near term peak in Dec 2016 and have slid 17% since then, there is a couple of noteworthy points.

Firstly, to put things in perspective, Ecocoal, at the Mar 2017 price of US$44.41, is still up approximately 45%, compared to one year ago. Secondly, the rate of monthly decline seems to be slowing. i.e. there is a possibility that it may trade sideways in the next few months. In KGI’s analyst report, they use a long term average selling price (“ASP”) of US$42 / tonne to derive their target price of S$0.960. As of now, coal prices are still trading above KGI’s long term ASP assumption.

Chart 2: Monthly coal price chart by brands

Source: Coalspot.com (27 Mar 17)

Chart analysis

With reference to Chart 3 below, GEAR is testing the support area of around $0.510 – 0.520. After the sharp drop post its listing on 12 Dec 2016, there seems to be a short to medium term uptrend as depicted by the uptrend line. However, a break below $0.510 on strong volume and on a sustained basis is negative for the chart.

Near term supports: $0.515 / 0.510 / 0.500

Near term resistances: $ 0.525 / 0.535 – 0.545 / 0.565 – 0.570

Chart 3: GEAR is testing the support at 0.510 – 0.515

Source: Chartnexus as of 27 Mar17

Conclusion

GEAR continues to lag behind Geo Energy in term of share price. This may be due to the market’s unfamiliarity with GEAR. Hopefully, this will be resolved to some extent by its continual delivery on its results (supported by a positive macro outlook), coupled with its investment seminars and site visit.

Readers are advised to refer to GEAR’s website (click HERE), the announcements on SGX, KGI research report and my previous write-up (click HERE) for more information.

Disclaimer

Please refer to the disclaimer HERE

Great blog.Thanks Again. Will read on…

Looking forward to reading more. Great blog.Really thank you! Cool.

Major thankies for the article.Much thanks again. Will read on…

I loved your blog article.

Thanks for sharing, this is a fantastic article.Really looking forward to read more. Much obliged.

I really liked your post. Cool.

I really like and appreciate your post.Really looking forward to read more. Want more.

Very good blog article.Really looking forward to read more. Really Great.

Appreciate you sharing, great article.

Really informative blog.Much thanks again. Really Cool.

I think this is a real great blog. Keep writing.

Very good blog post.Really looking forward to read more. Keep writing.

Thanks-a-mundo for the blog article. Really Great.

Really appreciate you sharing this article post.Thanks Again. Cool.

Thanks for sharing, this is a fantastic blog article.Much thanks again. Great.

Thanks again for the article post.Really looking forward to read more. Will read on…

Very neat post.Really looking forward to read more. Great.

I am so grateful for your post. Will read on…

A big thank you for your post. Fantastic.

Wow, great post.Really looking forward to read more. Want more.

Appreciate you sharing, great blog article.Much thanks again. Cool.

A big thank you for your post.Much thanks again. Will read on…

Im grateful for the article. Fantastic.

Thanks so much for the blog article.Much thanks again. Awesome.

Thanks a lot for the blog. Keep writing.

Major thanks for the blog.Really looking forward to read more. Fantastic.

I really like and appreciate your blog post. Keep writing.

I truly appreciate this blog post. Really Great.

Thanks again for the article post.Thanks Again. Will read on…

Really enjoyed this post. Fantastic.

Great, thanks for sharing this post.Really looking forward to read more. Want more.

Really enjoyed this article post.Much thanks again. Awesome.

Really appreciate you sharing this blog article.Much thanks again. Fantastic.

I loved your blog post. Want more.

Thanks so much for the post.Really thank you! Really Cool.

I am so grateful for your article.Really looking forward to read more.

Thank you for your post.Really looking forward to read more. Really Great.

I value the blog.Much thanks again.

Very neat article post.Really thank you! Want more.

Thank you ever so for you article post.Really thank you! Much obliged.

Major thanks for the article post. Fantastic.

Thanks a lot for the article post.Thanks Again. Much obliged.

Fantastic article post.Really thank you! Much obliged.

Awesome post.Really thank you! Fantastic.

Major thankies for the blog article.Much thanks again. Great.

I value the blog.Much thanks again. Keep writing.

Very informative blog.Thanks Again. Will read on…

Very good blog. Much obliged.

Great article post.Really looking forward to read more. Fantastic.

A big thank you for your article.Thanks Again. Keep writing.

wow, awesome blog post.Really looking forward to read more. Great.

Thanks so much for the article post.Really looking forward to read more. Cool.

Appreciate you sharing, great post. Much obliged.

Really appreciate you sharing this post.

A round of applause for your blog post.Much thanks again. Want more.

Enjoyed every bit of your blog.Really thank you! Will read on…

I loved your blog post.Much thanks again. Great.

I am so grateful for your blog.Thanks Again. Keep writing.

I really liked your blog.Thanks Again. Much obliged.

I value the article post.Much thanks again. Great.

Awesome blog article.Thanks Again. Really Great.

Thanks-a-mundo for the article.Much thanks again. Will read on…

Im thankful for the article post.Really thank you! Fantastic.

I really like and appreciate your article post. Great.

Thank you for your post.Really thank you! Fantastic.

Really informative blog post.Really thank you! Want more.

Major thankies for the article.Really thank you!

Really informative article post.Really looking forward to read more. Awesome.

Appreciate you sharing, great blog article.Thanks Again. Keep writing.

Thank you ever so for you blog.Thanks Again. Fantastic.

Im thankful for the article post.Really thank you! Want more.

Thanks-a-mundo for the article.Much thanks again. Want more.

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

I am so grateful for your blog post.Thanks Again. Much obliged.

A round of applause for your blog post.Thanks Again. Keep writing.

Major thanks for the post.Much thanks again. Want more.

Major thanks for the blog.Thanks Again. Cool.

Thanks for sharing, this is a fantastic blog.Really looking forward to read more. Awesome.

I really liked your blog post.Much thanks again. Fantastic.

Really informative article post.Much thanks again.

Enjoyed every bit of your post.Really looking forward to read more. Cool.

Im grateful for the blog.Really thank you! Great.

Appreciate you sharing, great blog post.Much thanks again. Really Great.

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Really informative article.Thanks Again. Much obliged.

I really enjoy the article post.

Thanks again for the blog article.Really looking forward to read more.

Really appreciate you sharing this post. Really Great.

Thanks so much for the post.Really thank you! Much obliged.

I really liked your article. Really Great.

I am so grateful for your blog article. Keep writing.

Awesome article post.Much thanks again. Keep writing.

Looking forward to reading more. Great blog post.Really looking forward to read more.

I think this is a real great blog. Awesome.

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Really enjoyed this post.Thanks Again. Really Cool.

Thanks again for the post.Much thanks again. Really Great.

Thanks so much for the post.Really looking forward to read more. Keep writing.

I think this is a real great article.Thanks Again. Great.

Appreciate you sharing, great blog post.Thanks Again. Really Cool.

I really enjoy the blog article.Much thanks again. Much obliged.

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

wow, awesome article post. Awesome.

A round of applause for your article.Really thank you! Fantastic.

Fantastic blog.Really thank you! Awesome.

I really liked your article post.Much thanks again. Really Great.

Im grateful for the article.Much thanks again. Cool.

The THC concentrations in CBD Guru products are below detectable levels. These THC-free broad-spectrum CBD Gummies will never flag a drug test. The reason for this is simple: no one tests for CBD. Athletes can use it in the Olympics, the elderly are thriving on these products, and plenty of people are only taking these products to enhance their daily lives. There is no penalty for taking a thoroughly tested and carefully formulated cannabidiol product. Your mind and body will thank you, and local law-enforcement agents recognise the legal availability of these hemp items. You never need to worry when purchasing a CBD gummy product.

This is one awesome post.Thanks Again. Really Cool.

Whether you’re a seasoned CBD enthusiast or just beginning your wellness journey, CBD Guru’s CBD Gummies are the perfect companion. Boost your daily routine with a burst of flavour and the holistic benefits of high-quality CBD. Shop with confidence, knowing you’re choosing a product that’s crafted with expertise and a commitment to your well-being. Correctly manufactured CBD sweets should never get you high. These products must be extracted from industrial hemp, which contains inactive amounts of THC. Without THC, these items will remain non-psychoactive and buzz-free. Consulting lab-test results is always an essential step before purchasing cannabidiol. If you can lock-eyes on results indicating a pure, and THC free product, then you run zero risk of catching a buzz. CBD Guru’s broad-spectrum formula contains viable levels of many hemp compounds but does not contain detectable amounts of THC. Get to know your supplier, and learn to read CBD lab test results. This only takes a little bit of effort, and if it ensures that you will have access to quality cannabidiol. We guarantee that it is worth your time. Support this budding industry by learning about CBD, browsing the highest quality goods, and discovering how to choose the best cannabidiol items on the market. The THC concentrations in CBD Guru products are below detectable levels. These THC-free broad-spectrum CBD Gummies will never flag a drug test. The reason for this is simple: no one tests for CBD. Athletes can use it in the Olympics, the elderly are thriving on these products, and plenty of people are only taking these products to enhance their daily lives. There is no penalty for taking a thoroughly tested and carefully formulated cannabidiol product. Your mind and body will thank you, and local law-enforcement agents recognise the legal availability of these hemp items. You never need to worry when purchasing a CBD gummy product. At first, many customers may have asked themselves, “Is it legal to buy CBD Gummies in the UK?” The answer is an absolute yes. The UN WHO (World Health Organisation) has stated that products containing under 0.2 THC should be distributed freely. Regulators in the UK have not classified CBD as a food, cosmetic, or medicinal, indicating that it can be bought and sold without issue. The hemp used to create these tasty treats are all grown in Colorado, a state notorious for its legal cannabis and hemp cultivation. These premium plants are held to the high standards of the CO state regulations. The plant material is processed and infused into our premium products in GMP facilities that produce food-grade products.The importation of these hemp products is legal, while the extraction of cannabinoids from any hemp plant is still not allowed in the UK. Although the nation is turning to other sources to procure its medicinal cannabis and hemp supply, there will be a wait before we can cultivate our own UK grown plants. In the meantime, we choose farmers who uphold the best organic and sustainable hemp farming practices. Using CBD sweets & gummies is an easy task. All you need to do is to savour and eat these delicious products to get your daily dose. You can eat these back to back, but pay attention to the dosage. We know that the flavour of our gummies can be quite enticing, but you may want to save your gummies and eat only the minimum effective dose. Before purchasing these items, check the amount of total CBD mg in your selected package and the CBD mg amount of individual pieces. If you are buying CBD for the first time, start with pieces with low mg amounts such as 20mg gummies. This will allow you to easily explore various dosages and find out how your body responds.

1. CBD gummies are quick, fun and easy

A big thank you for your post. Cool.

I value the article post. Want more.

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ

Hi, It has come to our attention that you are using our client’s photographs on your site without a valid licence. We have already posted out all supporting documents to the address of your office. Please confirm once you have received them. In the meantime, we would like to invite you to settle this dispute by making the below payment of £500. Visual Rights Group Ltd, KBC Bank London, IBAN: GB39 KRED 1654 8703, 1135 11, Account Number: 03113511, Sort Code: 16-54-87 Once you have made the payment, please email us with your payment reference number. Please note that a failure to settle at this stage will only accrue greater costs once the matter is referred to court. I thank you for your cooperation and look forward to your reply. Yours sincerely, Visual Rights Group Ltd, Company No. 11747843, Polhill Business Centre, London Road, Polhill, TN14 7AA, Registered Address: 42-44 Clarendon Road, Watford WD17 1JJ