Dear all

Singapore Post Limited (SingPost) is one of CGSI’s three value picks with re-rating potential in their Singapore Strategy report dated 8 May 2024. I have the privilege of meeting SingPost Group CFO, Mr Vincent Yik this month which I have shared with my LinkedIn (click HERE). It is interesting that SingPost has formed a potential bullish hammer on 28 June with a one-month high volume.

SingPost closed at $0.430 on 28 Jun 2024.

Why is SingPost interesting? I have summarised my readings from SGX announcements, analyst reports and my 1-1 interaction with Vincent in this article. Some key noteworthy points are that SingPost may achieve strong underlying net profit growth in FY25F and this potential bullish hammer formation on last Friday may indicate a near term bottom in share price.

Read on for more below.

Description of its business segments

SingPost is a leading postal and eCommerce logistics provider in Asia Pacific. The portfolio of businesses spans from national and international postal services to warehousing and fulfilment, international freight forwarding and last mile delivery, serving customers in more than 220 global destinations.

Headquartered in Singapore, SingPost has over 4,900 employees, with offices in 13 markets worldwide. Since its inception in 1858, the Group has evolved and innovated to bring about best-in-class integrated logistics solutions and services. Readers can refer to SingPost website HERE for more information.

Interesting observations

a) Australia operations – Tremendous opportunities from numerous aspects

Australia poses tremendous opportunities for SingPost from numerous aspects.

Firstly, with the acquisition of Border Express, SingPost is among the top 5 integrated logistics service operators in Australia by revenue. In SingPost’s latest FY24 results, there was only one month of contribution from Border Express which contributes AUD25m in revenue and operating profit of AUD2.5m. If I just annualise it simplistically, ignoring factors such as seasonality cross-selling opportunities and cost savings and assuming all things remain equal, SingPost should be able to recognise AUD300m in FY25F revenue and AUD30m in FY25F operating profit. To put this into perspective, SingPost’s FY24 revenue and operating profit were S$1.7b and S$84.9m respectively.

Secondly, SingPost has further increased its stake in Freight Management Holdings to 100% which should augment its earnings in FY25F.

Thirdly, there are tremendous cross selling opportunities especially when SingPost can tap onto Border Express’ customers which they previously don’t have access to. Furthermore, SingPost can also enjoy higher economies of scale as their size increases.

Fourthly, besides economies of scale, there are substantial cost savings to be reaped. Just to cite an arbitrary example, SingPost may be using trains to move their pallets at 70% capacity. Border Express runs trucks approximately 70% occupancy. For example, they can reduce Border Express occupancy by 30% and move the items via trains to raise it to close 100% occupancy, then they would have saved on expenses. In addition, SingPost may be able to do uniform purchases of items on an enlarged scale which may drive costs down. Furthermore, integration of back-office operations may be another angle to reduce costs.

On the cost savings aspect, CGSI estimates that SingPost can derive cost savings of around S$25m in the next two FYs even without considering cross selling potential.

Fifthly, on 21 Jun 2024, SingPost appointed Merrill Lynch Markets Australia Pty Limited as financial advisor to the Board to formulate optionalities for the Group’s Australia business specifically. To recap, based on SingPost’s 19 March 2024 announcement, one of the strategic thrusts of the Group is to achieve scale in Australia by exploring near term partnerships that contribute to growth, providing equity to deleverage acquisition debt and establishing an independent valuation benchmark, as well as continuing to pursue appropriate M&A opportunities and seek future liquidity options to maximise value.

b) Largest in 4PL business in Australia, bigger than 3-4 of their next competitors combined!

Although SingPost is now among the top 5 integrated logistics service operators in Australia by revenue, SingPost believes that they are the largest player in fourth party logistics (4PL), bigger than the next 3-4 of their Australia peers put together. See Figure 1 on the services which a 4PL generally provides.

Figure 1: Services provided by 4PL players

Source: A.P. Moller-Maersk Group

According to SingPost, their platform does the analytics given customers’ requirements and vendor capacities and abilities, and the system then gives the recommendations based on e.g. pricing, routing, service, delivery. The 4PL operations are run by data analysts which are different from that of a traditional logistics business. As such, SingPost believes this segment has the best defensive margins due to their value add as customers can just liaise with them as the main point of contact. SingPost will then liaise with the different 3PL players. SingPost even has its own 3PL players which can act as providers of last resort. Furthermore, SingPost sees growth potential in this segment as customers gradually understand the value add which 4PL players can bring onto the table. For the customers perspective, they should get the lowest costs on an overall basis if they engage a competent 4PL player, rather than if the customers go out to find the individual services.

Readers can click HERE where A.P. Moller-Maersk Group, the largest shipping company seeks to explain the difference between 1PL, 2PL, 3PL and 4PL.

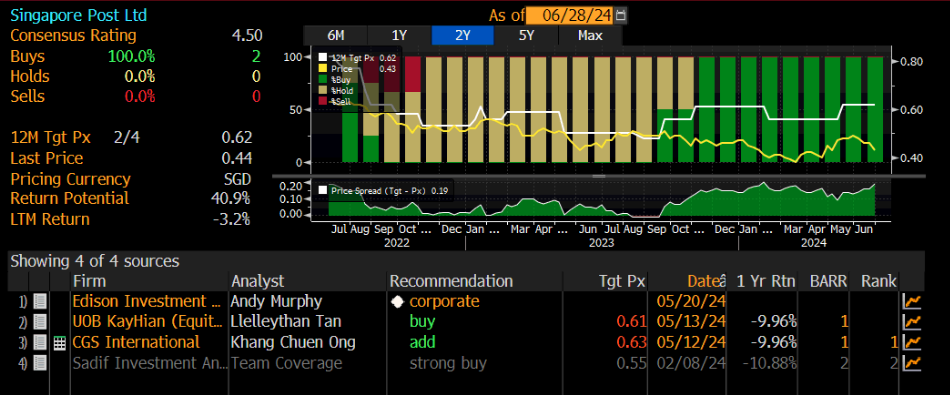

c) Analysts are generally positive with an average target price $0.620

Based on Figure 2 below, average analyst target price is around $0.620. Inclusive of an estimated FY25F dividend yield of around 3.0%, this translates to a total potential return of 47% should the consensus be right.

It is noteworthy that there are only two rated analyst reports on SingPost. As at 30 May 2024, Temasek has 22.0% deemed interest in SingPost through its subsidiary, Singapore Telecommunications Limited, and its associated company, DBS Group Holdings Ltd. For a Temasek linked company with a market capitalisation of $967.5m; coupled with improving business fundamentals, earnings profile and dividends, I suspect it is a matter of time before SingPost sees more rated analyst coverage.

Figure 2: Average analyst target price $0.620; total potential upside is around 47%!

Source: Bloomberg 28 Jun 24

d) Chart: Potential bullish hammer formation

Based on Chart 1 below, SingPost has retraced approximately 50% from its up-move $0.375 – 0.505. It closed at $0.430 on last Friday. Day range was $0.415 – 0.435. Based on chart, it has formed a potential bullish hammer formation. On balance, this looks encouraging especially when

- The hammer formation is accompanied with a one-month high volume. I suspect this high volume is partly attributed to some contra players who may have entered on 21 June and may have to either exit or roll their positions. Furthermore, 28 Jun is the last day of the calendar quarter and first half of the year hence there may be funds doing rebalancing, or / and window dressing;

- Price has retreated to a strong support region $0.420 – 0.430. This level is the former breakout level and Fibonacci level which should see some buying interest;

- RSI closed 32.3 and is approaching oversold level.

Nevertheless, it is noteworthy that SingPost is still on a downtrend established since Apr 2019 and it faces strong near-term resistance around $0.450 – 0.460.

Chart 1: SingPost forms a potential bullish hammer formation

Source: InvestingNote 28 Jun 24

e) Divestment opportunities worth approximately S$200m in the near term

In SingPost’s strategic review unveiled on 19 Mar 2024, SingPost has identified a list of assets and businesses that are non-core to its strategy which can be monetised to recycle the capital. This includes selected properties as well as various assets in its international footprint. Potential proceeds will be appropriately allocated by the Board to reduce debt, support growth investments, and return value to shareholders.

Short to medium term – divestment targets

Two potential “low hanging fruits” in SingPost’s divestment strategy may be 4PX and Famous Holdings.

Based on this Straits Times article dated 20 Jan 2023 (click HERE), SingPost’s subsidiary Quantium Solutions International (QSI) has been granted two put options to sell its equity interest in 4PX to Cainiao worth approximately S$96m.

Secondly, Famous Holdings is also one of the non-core holdings which analysts have highlighted to be potential targets for divestment.

Both of the above divestments, if materialise, may fetch combined proceeds amounting approximately S$200m.

Over the medium to long term

SingPost centre, valued to be around S$1.13b on the books may also be one of the potential divestment targets. If it materialises, it will likely to have a significant impact to SingPost.

However, being a “larger ticket item”, I suspect this potential divestment may take more time. Furthermore, the current property market and interest rate environment may not be super conducive to extract the best value yet.

Another potential value unlocking exercise may be its Australia business. As mentioned above, on 21 Jun 2024, SingPost appointed Merrill Lynch Markets Australia Pty Limited as financial advisor to the Board to formulate optionalities for the Group’s Australia business specifically (see above pt a for more information).

All in, as SingPost commences its strategic transformation, CGSI estimates that it may have S$2.5b worth of assets, slated for value unlocking in the next 3 years. To put this into perspective, at the moment, SingPost’s market capitalisation is around S$967.5m at the closing price of $0.430 on 28 Jun 2024.

f) AGM is on 24 Jul

SingPost will be hosting their AGM in a hybrid format at Suntec Singapore Convention & Exhibition Centre, Level 3, Summit 1 and using virtual meeting technology on 24 Jul 2024, 230pm. In line with their past practice, I suspect SingPost may do a presentation of their business to their shareholders at the AGM. Shareholders are encouraged to attend its physical AGM to meet SingPost’s management and directors.

g) FY24 dividend is $0.0074 / share; consensus expects a hike of 76% to $0.013 / share in FY25F

SingPost will ex-div $0.0056 / share on 31 Jul 2024. For FY24 (financial year ends on 31 Mar), SingPost’s total dividend per share amounts to around $0.0074, or 40% of the underlying net profit. Based on Bloomberg, consensus estimates that SingPost may be able to give out $0.013/ share for FY25F, translating to a 76% hike in dividends on a year-on-year basis.

Important noteworthy risks

Besides the usual business, geopolitical, forex and macro risks, some other risks may be:

a) Chart reading is subjective and stock can get lower

It is important to note that chart reading is subjective. Furthermore, sometimes in selling climaxes, hammers appear frequently. Thus, for the hammer formation to be valid, it is good to wait for a bullish confirmation, either in the form of a gap up or long green candle with above average volume.

b) Limited analyst coverage

Although SingPost’s market cap is around $968m, it only has two rated reports with active coverage (See Figure 2 above). Notwithstanding this, under-researched companies may arguably have higher potential return if they continue to execute well for their shareholders.

c) My first time looking at SingPost – may not have covered all angles

This is my first time looking at SingPost after several years. In the interest of time, I may, and most likely have not covered all angles on SingPost. Readers are encouraged to view the various announcements posted on SGX (click HERE). Readers are also advised to refer to SingPost’s analyst reports HERE to appreciate more about the specific investment merits and risks on SingPost.

d) Potential share overhang from Alibaba’s recent sale at $0.460 / share

Based on the SGX announcement posted on 7 June 2024, Alibaba Investment, a subsidiary of Chinese e-commerce giant Alibaba Group, sold 72.5m shares in SingPost for S$33.3m on 7 June 2024. This works out to be an average price of around $0.4593 / share. With this sale, Alibaba Investment’s stake in SingPost is trimmed to around 11.3%, or around 255.1m SingPost shares. Thus, there may be some share overhang as markets may be wary of future sales by Alibaba.

e) May need several quarters to convince skeptics

SingPost has fallen from an intraday high of $2.15 on Jan 2015 to trade $0.430 last Friday. Excluding dividends earned since then, SingPost has fallen a whopping 80.0%. Thus, it is natural for the investment community to be sceptical on whether SingPost can deliver and execute on its plans. Naturally, this takes time to assess.

Conclusion

In summary, SingPost may be on a strong earnings recovery path due to the afore-mentioned points. In fact, FY25F underlying net profit may post a sharp jump of 71.7% on a year-on-year basis should the consensus be right. Furthermore, the fact that SingPost is only covered by two rated brokerage reports seems to indicate that this potential earnings recovery play may not have been fully noticed by the market.

Besides the usual business, geopolitical, forex and macro risks and the above risks discussed, the pertinent risk (or at least at the top of my mind) is the potential share overhang by Alibaba. Nevertheless, if SingPost sells off due to this reason, it may arguably be a buying opportunity for the patient as long as SingPost continues to deliver on its results and plans.

To reiterate, readers are encouraged to view the various announcements posted on SGX (click HERE). Readers are also advised to refer to SingPost’s analyst reports HERE to appreciate more about the specific investment merits and risks on SingPost.

Readers who wish to be notified of my write-ups and / or informative emails, can consider signing up at http://ernest15percent.com. However, this reader’s mailing list has a one or two-day lag time as I will (naturally) send information (more information, more emails with more details) to my clients first. For readers who wish to enquire on being my client, they can consider sending an email to my email address

Readers can refer to my LinkedIn HERE to see my activities and which companies I have met on a 1-1 basis.

P.S: I am vested. I have also informed my clients to take a look at SingPost late last week.

Disclaimer

Please refer to the disclaimer HERE

You should take part in a contest for one of the best blogs on the web. I will recommend this site!

I like the valuable information you provide in your articles. I’ll bookmark your blog and check again here frequently. I’m quite sure I will learn many new stuff right here! Best of luck for the next!

Попробуй свою удачу в 1win казино, становись богаче.

Увлекательные слоты в 1win казино, подарят незабываемый опыт.

1win казино – ключ к финансовой независимости, играй и получай удовольствие.

Играй и побеждай вместе с 1win казино, получай крупные выигрыши.

1win казино – место, где рождаются победы, подари себе азарт и адреналин.

Наслаждайся азартом без ограничений в 1win казино, забирай свой джекпот.

1win казино – это место, где рождаются чемпионы, претворить свои мечты в реальность.

Удовольствие и адреналин в 1win казино, гарантировано доставит тебе радость.

1win вход 1win вход .

loli cp

==> biturl.top/qeAJJf rlys.nl/6epap3 <==

Hey people!!!!!

Good mood and good luck to everyone!!!!!