Dear all

On 11 Jan, Comfort (CD) closed at $1.21, the lowest close since 31 Oct 2008. The next day, to the horror of CD’s shareholders, it broke $1.21 with volume expansion and closed at $1.18. At the time of this write-up, CD closed today at $1.14, the lowest close last seen 29 Oct 2008.

Will CD fall more? Or will this be a comfortable trade at current level? Let’s read on for more.

Possible reasons to be bullish

A) Still a recovery play

CD with its operations in Australia, China, Singapore, UK etc. should gradually benefit as economies re-open. China’s abrupt easing of its Covid measures will likely facilitate more commuting and travelling in China and outside China.

Based on Bloomberg, the consensus from analysts is still projecting CD to post a year-on year (“y-o-y”) net profit growth of 30% in FY22F; 16% in FY23F; 7% in FY24F. Thus, suffice to say that CD is still a recovery play and is likely to post year on year profit growth. Much cannot be said for some companies as they may report a y-o-y drop in net profit in FY23F especially if their FY22F is an exceptional year.

B) Valuations are incredibly low; 2.0x standard deviations below its average 10Y P/BV

Based on Bloomberg, CD trades at 2.0x standard deviations below its average 10Y P/BV of 1.9x. With net profit expected to rise in FY22F, FY23F and FY24F (see point A above), it does not seem justifiable to trade at such depressed valuations.

C) Net cash $647m; easily can finance M&A & 5-6% dividend yields

Based on some of the analyst reports which I have read, CD’s balance sheet has emerged stronger after the pandemic. CD has net cash amounting to $647m in 3QFY22 vs $520m in 4QFY21. In other words, 26% of market cap is backed by net cash. Such strong balance sheet should be able to support its dividends and any acquisitions. Furthermore, generally speaking, in a rising interest rate environment, having net cash is better than being in debt.

D) 14-year low price since 29 Oct 2008

During the height of the pandemic, CD traded to a low of around $1.30 – 1.31. At that time, the economy and human traffic come to an almost standstill and plagued with uncertainties on how the pandemic will pan out. It is difficult to see how its operations can be worse now compared to the pandemic. Granted that analysts have cut their profit estimates for CD, the consensus net profit still expects CD to post a 30% rise in FY22F; 16% in FY23F; 8% in FY24F.

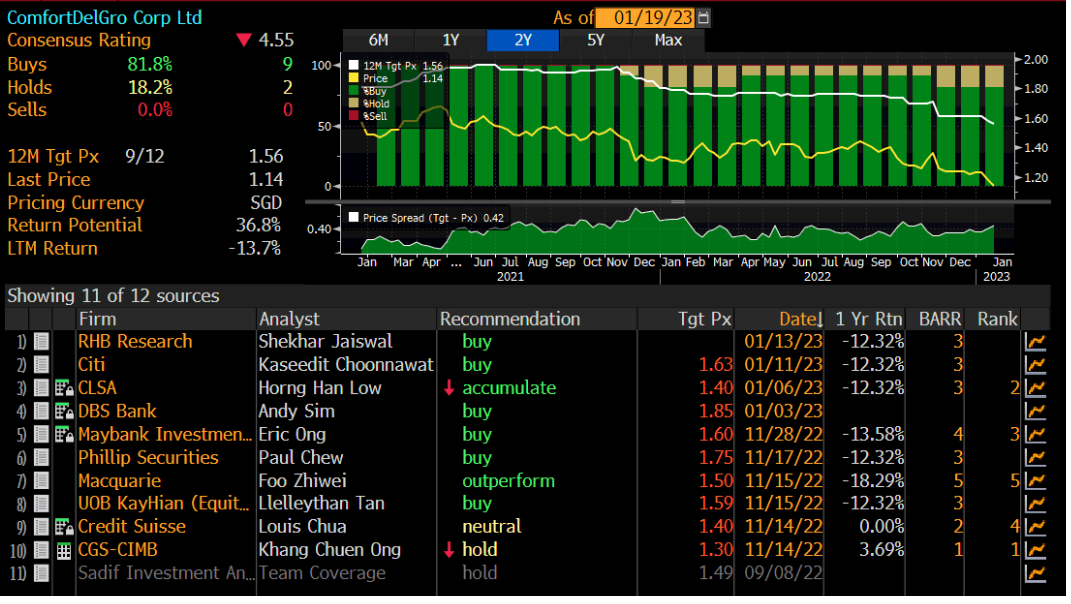

E) Total potential upside is around 43% if the consensus is right

Based on Bloomberg, average analyst target price is $1.56; FY23F estimated div yield is at 6.0%. If the consensus is right, CD presents a total potential return of around 43%.

Figure 1: Analyst target prices for CD at $1.56

Source: Bloomberg 19 Jan 23

Possible risk factors to be cautious

A) Overseas operations may face headwinds from competition, narrowing margins + forex risks

Based on Maybank 15 Nov 2022 report, overseas operations were below expectations due to forex effects; inflationary cost pressures; driver shortage and the timing mismatch to pass on the higher costs (public bus services fees see indexation from wage and CPI on an annual basis).

B) Risk of catching a falling knife

Notwithstanding CD’s attractive valuations, it is noteworthy that stocks can always go lower. This is why some market watchers advise against catching a stock which is falling. Catching a stock which is free-falling is especially dangerous for small mid cap stocks. Personally, for large cap stocks, this risk is slightly less as it is usually widely covered by analysts and there should theoretically be less blind spots. Nevertheless, I hasten to add that this depends on one’s strategy and risk profile.

Based on my pure personal observation of price action and chart, there seems to be buying interest around $1.14.

C) Risk of economy closure should there be another pandemic

In the event that there are lockdowns again, there will be an adverse effect on CD’s business operations.

D) UK operations – constant strikes may affect CD’s UK operations

There is a possibility that the constant strikes in UK may have an effect on CD’s UK operations (click HERE). Based on Sky News, 70,000 members of the University and College Union (UCU) will join civil servants, teachers and train drivers etc. on 1 Feb 2023 for strikes.

Personally, I do not know whether such strikes will have any material effect on CD’s UK operations. However, at the very least, it does not aid in investor sentiment in CD.

E) AirAsia plans to expand the ride-hailing service to Singapore by June this year

Based on an article in CNA (click HERE), AirAsia through Capital A plans to launch its ride-hailing service to Singapore by June this year. There is a possibility that investors may be worried on the potential competition which is a valid concern. However, I personally feel with the experience of dealing with competition from Grab, CD is likely to be better positioned this time.

F) Such large volume sell offs may be a result of a change in positioning by the institutions

Since 11 Jan, CD has traded in excess of 8m of shares per day. Such large volume transactions may be a result of a change in positioning by the institutions. If this is really the case, we do not know how many shares they are prepared to sell at current 14 year low prices.

G) May have other reasons which caused this fall

There may be reasons known to some people in the market but unknown to me which cause CD’s share price to decline on large volumes.

Conclusion

It is noteworthy that there are risks involved such as the aforementioned risks (e.g. potential competition from AirAsia, headwinds facing its overseas operations etc.). Nevertheless, CD at 14-year low price; valuations trading at 2 standard deviations below its 10Y average P/BV; net cash and 6.0% FY23F estimated dividend yield, I am comfortable to take some risks in accumulating CD for a trading play.

For a more complete picture, it is advisable to refer to CD’s analyst reports (Click HERE); SGX website (Click HERE) and CD’s corporate website (Click HERE).

Readers have to assess their own % invested, risk profile, investment horizon and make your own informed decisions. Everybody is different hence you need to understand and assess yourself. The above is for general information only. For specific advice catering to your specific situation, do consult your financial advisor or banker for more information

Readers who wish to be notified of my write-ups and / or informative emails, can consider signing up at http://ernest15percent.com. However, this reader’s mailing list has a one or two-day lag time as I will (naturally) send information (more information, more emails with more details) to my clients first. For readers who wish to enquire on being my client, they can consider leaving their contacts here http://ernest15percent.com/index.php/about-me/

Lastly, in line with my usual practice of compiling SGX stocks sorted by total potential return at the start of the month, readers who wish to receive my manual compilation of stocks sorted by total potential return can leave their contacts here http://ernest15percent.com/index.php/about-me/. I will send the list out to readers around 4-5 Feb 2023.

P.S: With reference to my earlier write-up (click HERE), I have previously taken profit when CD traded $1.34-1.38 just before it released 3QFY22 results in Nov. I have bought back CD for the past few days for a potential trading play.

Disclaimer

Please refer to the disclaimer HERE

I highly recommend Devon . Briansclubcm.to to anyone looking to improve their online presence.

Great write..

Good write.. awesome.

We’ve seen a significant increase in website traffic and brianclubcm.cc conversions since working with PPC Birmingham.

If you’re looking for a professional and experienced social media agency, briansclub I highly recommend the one in Derby.

We’ve seen a significant improvement in our online visibility since working with the https://brianclubcm.cc/ PPC team in Birmingham.

In the dynamic world of digital marketing, where the competition for online visibility is fierce, understanding and implementing effective Search Engine Optimization (SEO) strategies is crucial for businesses aiming to succeed online. SEO serves as the cornerstone of online marketing, enabling websites to enhance their visibility, attract organic traffic, and ultimately achieve their business objectives. In this article, we delve into the realm of search engine optimization, exploring its significance, key principles, and actionable strategies for maximizing online visibility. https://bit.ly/3JKYpu5

A combination of cutting-edge techniques and strategic insights that propel your website to the forefront of search engine results. From on-page optimization to off-page tactics, every aspect of our formula is designed to maximize your website’s visibility and drive targeted traffic. https://bit.ly/3JKYpu5

DISCOVER THE HIDDEN KEY TO ONLINE SUCCESS WITH OUR SECRET SEO FORMULA https://bit.ly/3JKYpu5

Good write..

whoah this weblog is great i really like reading your articles Keep up the great paintings! You already know, a lot of people are searching around for this info, you could aid them greatly

Master SEO and Skyrocket Your Website’s Traffic! Download our free eBook, “The Ultimate Guide to SEO,”