Merry Xmas!

As we approach end 2019, most market strategists are putting their market estimates for end 2020. Although I do not profess to be in the league of these market strategists, just for fun, I am expecting STI to head towards 3,390 in 1Q2020. STI closed at 3,222 on 24 Dec 2019. I have outlined my basis and the risks involved.

Factors for my bullish basis

a) Chart looks positive after bullish break

Based on Chart 1 below, STI has staged a bullish break above its flag formation on 12 Dec 2019. Notwithstanding below average volume for the past couple of weeks (perhaps due to holiday period) and low ADX, STI’s indicators are slowly strengthening with rising OBV, MFI and RSI. The bullish break on 12 Dec points to an eventual technical measured target of around 3,389, probably in the next 1-3 months. Based on the chart development, STI is likely to breach its 200-day exponential moving average, currently around 3,224 soon. A sustained break below the upper channel line of the flag formation will negate the bullish picture.

Near term supports: 3,208 / 3,198 / 3,188 / 3,175

Near term resistances: 3,224 / 3,232 / 3,250 / 3,286

Chart 1: Bullish break above flag

Source: InvestingNote 24 Dec 19

b) Positive developments on the trade war

President Trump said last Saturday that he expects to sign Phase 1 Trade Deal with China “very soon.” This comes on the back of a phone call between U.S. and China last Friday. An easing of U.S. / China trade tensions is likely to boost risk on sentiment, at least in the near term.

c) Signs of growing global economic stabilization in the short term

Most economic data seem to be stabilising. For example, China has reported stronger than expected PMI, industrial production and retail sales data. U.S. housing permits are strong in the U.S. at a 12-year high with unemployment rate at near 50-year lows. Although there are still pockets of weakness in certain economic data such as core durable goods, U.S. manufacturing PMI etc., suffice to say that there are signs of growing global economic stabilization in the short term.

d) Singapore equity market is likely to be better in 2020 due to several factors below

Based on various analyst reports, it is likely that Singapore’s manufacturing sector should be bottoming, evidenced by rising global semiconductor shipments and improvement in semiconductor equipment billings. This is also in line with the anticipated recovery in the global electronics cycle. Based on a DBS Research report dated 12 Dec 2019, DBS postulates that Singapore’s 2020 GDP to improve to 1.4% year on year from 0.6% this year. Coupled with a likely expansionary 2020 fiscal budget (election coming), this is likely to buoy market and sentiment.

Furthermore, STI’s valuations are cheap compared to historical standards. STI’s P/BV is at 1.1x vis-a-vis its 10Y average P/BV of around 1.3x. It also compares favourably against S&P500’s 3.6x P/BV and Hang Seng’s 1.2x P/BV. Singapore market may see a re-rating, should our macroeconomic picture improve.

In addition, our Singapore market is backed by 4.1% estimated dividend yield which is one of the highest in Asia and should cushion downside risk to some extent.

Risk factors

Notwithstanding the above bullish factors, there are noteworthy risks on the horizon. Below are just some examples of risks which we should be cognisant of.

a) China corporate debt and record rate of defaults

According to Moody Analytics, they believe that China’s burgeoning corporate debt which may lead to more corporate defaults amid the slowdown in their economy in 2019. In a Reuters’ article dated 10 Dec 2019, Fitch Ratings mentioned that China has seen defaults from its corporate issuers totalling RMB99.4b in the first 11 months of 2019. Fitch also said that 2020 may also see such defaults as companies face pressure from a slowing economy. Thus, it is likely that this is one of the risks which may keep fund managers awake at night.

b) Geopolitical risks remain

Geopolitical risk is also one of the risks that remains on the horizon. Such risks can sprout from several areas. For example, North Korea has promised to send a “Christmas Gift” unless U.S. adheres to an end of year deadline to give concessions to North Korea.

In addition, the protests in Hong Kong have already been into their sixth month. Any severe deterioration in the protests may lead to China enforcing more severe measures which may have repercussions on the overall market sentiment.

c) S&P500 valuations are high

Although valuations for Asian markets are not high, S&P500 valuations are high on a historical comparison. As of 20 Dec 2019, S&P500 trades at 21.5x current PE and 3.6x P/BV as compared to its 10-year average 17.9x PE and 2.7x P/BV. Such lofty valuations may indicate that much optimism has been baked into the share prices and leaves it prone to disappointments and profit taking. Any sustained weakness or profit taking in S&P is likely to have an adverse impact on our markets.

d) Trade war not over yet

Although U.S. and China have agreed in principal to Phase 1 of the trade deal, they are still crafting the legal text, and anything can happen during this process. Even if they sign, there are still many aspects for them to monitor, enforce and discuss going forward. Furthermore, there may be a Phase 2 or Phase 3 in the medium term. In addition, trade tensions between U.S. and EU may worsen in 2020, depending on their negotiation.

Conclusion

After assessing both the aforementioned positive and risk factors (note that they are not exhaustive), I am bullish in our Singapore market over the next couple of months and have raised my percentage invested to around 200% invested. (My clients are aware of what I’m vested in) I may increase my equity exposure if I find more interesting ideas.

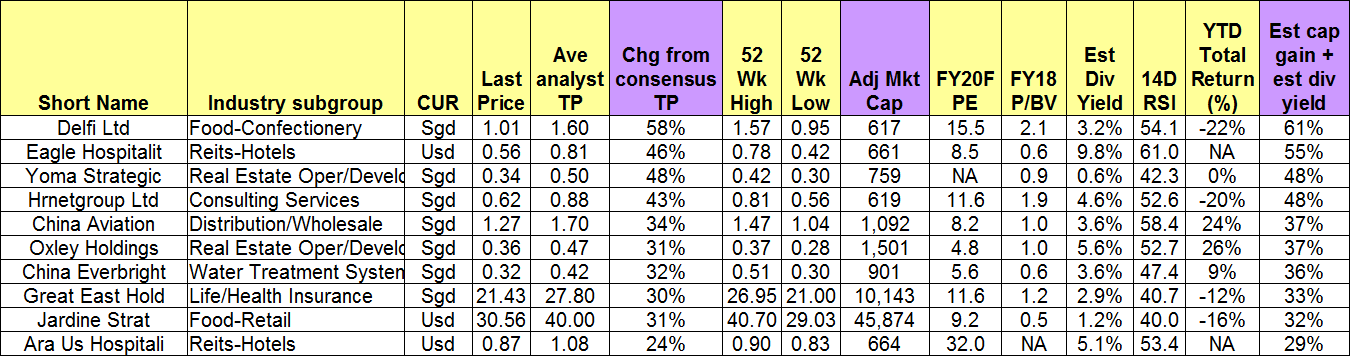

Using Bloomberg data as of 20 Dec 2019, I have compiled a list of stocks sorted by total potential return, based on the simple criteria below. For the purpose of this write-up, I have put in the top 10 stocks (Table 1) and bottom 10 stocks (Table 2) sorted by total potential return. (My clients will get the full list.). Delfi, Eagle Hospitality and Yoma Strategic are the top three stocks sorted by total potential return. Conversely, Mandarin Oriental, Hi-P and SGX are the bottom three stocks sorted by total potential return.

Table 1: Top 10 stocks sorted by total potential return

Source: Bloomberg; Ernest’s compilations

Table 2: Bottom 10 stocks sorted by total potential return

Source: Bloomberg; Ernest’s compilations

P.S: I am not vested in the above stocks listed in both Tables 1 and 2 above.

Criteria

1. Presence of analyst target price and estimated dividend yield;

2. Market cap >=S$500m.

Caveats

1. This compilation is just a first level stock screening, sorted purely by my simple criteria above. It does not necessary mean that Delfi is better than Eagle or Yoma Strategic in terms of stock selection;

2. Even though I put “ave analyst target price”, some stocks may only be covered by one analyst hence may be subject to sharp changes. Also, analysts may suddenly drop coverage;

3. Analyst target prices and estimated dividend yield may be subject to change anytime, especially after results announcement or after significant news announcements.

Readers who wish to be notified of my write-ups and / or informative emails, can consider signing up at http://ernest15percent.com. However, this reader’s mailing list has a one or two-day lag time as I will (naturally) send information (more information, more emails with more details) to my clients first. For readers who wish to enquire on being my client, they can consider leaving their contacts here http://ernest15percent.com/index.php/about-me/

Merry Xmas to all my readers / clients. To a better 2020 ahead!

*Important caveat

Portfolio investing is based on probability, weighted to the various scenarios, coupled with individual’s market outlook, risk tolerance, portfolio constraints, returns expectations etc. Naturally, my market outlook and trading plan are subject to change as markets develop and new information come in. My plan will likely not be suitable to most people as everybody is different. Do note that as I am a full time remisier, I can change my trading plan fast to capitalize on the markets’ movements (I am not the buy and hold kind). Furthermore, I wish to emphasise that I do not know whether markets will drop or continue to rebound. However, I am acting according to my plans. In other words, my market outlook; portfolio management; actual actions are in-line with one other. Notwithstanding this, everybody is different hence readers / clients should exercise their independent judgement and carefully consider their percentage invested, returns expectation, risk profile, current market developments, personal market outlook etc. and make their own independent decisions.

Disclaimer

Please refer to the disclaimer HERE

sumatriptan kopen in Duitsland aankoop van sumatriptan in Europa

Betrouwbare online apotheek voor sumatriptan

aankoop van slaappillen op basis van sumatriptan

apotheek die imitrex verkoopt sumatriptan online bestellen met snelle

levering

sumatriptan kopen in België zonder voorschrift

sumatriptan bestellen in Frankrijk Ontvang sumatriptan snel en eenvoudig bij u thuis in Nederland

imitrex zonder recept verkrijgbaar in Zwitserland sumatriptan kopen in België via internet

Beste plek om imitrex zonder recept te vinden imitrex kopen in Nederlandse apotheek

Goedkope imitrex zonder recept verkrijgbaar aankoop van slaapmiddelen imitrex

imitrex: een veilige en effectieve optie, nu online verkrijgbaar

imitrex vrij verkrijgbaar in België imitrex online bestellen:

veilig en vertrouwd

sumatriptan online kopen: veilig en snel

sumatriptan kopen bij apotheek vrij verkrijgbare imitrex in België

waar sumatriptan te vinden

online apotheek in Brussel voor sumatriptan

imitrex bestellen in Amsterdam

sumatriptan zonder voorschrift gemakkelijk verkrijgbaar in Nederland imitrex in België

sumatriptan bestellen in Rotterdam

Ontdek waar je sumatriptan online kunt vinden zonder voorschrift in Nederland.

sumatriptan op voorraad in Rotterdam aankoop van imitrex online